U.S Futures green - Watch INTC, PG, PM, IBM, GS, MRNA, MSFT

The S&P 500 Futures are posting a rebound after they closed sharply lower yesterday. Despite House Speaker Nancy Pelosi calling on the government to reconcile remaining disputes on a fiscal stimulus package within 48 hours, no progress was made toward a deal agreement between the government and Congress.

Later today, September housing starts (1.46 million units expected) and building permits (1.51 million units expected).

European indices are slightly bullish. The German Federal Statistical Office has posted PPI for September at +0.4% on month (vs -0.1% expected).

Asian indices closed in the red except the Chinese CSI.

WTI Crude Oil futures are posting a rebound. Later today, American Petroleum Institute (API) will release the change of U.S. oil stockpile data for October 16.

Gold and U.S dollar steady as investors await developments on U.S stimulus aid.

Gold rose 0.85 dollar (+0.04%) to 1904.93 dollars.

The dollar index fell 0.24pt to 93.188.

U.S. Equity Snapshot

Procter & Gamble (PG), a global manufacturer of consumer products, expects full year organic sales growth of 4%-5% vs a previous outlook of 2%-4% increase.

Philip Morris International (PM), a manufacturer of tobacco products, raised full year adjusted EPS guidance to 5.05-5.10 dollars from 5-5.07 dollars previously. Third quarter adjusted EPS was 1.42 dollar, beating estimates, vs 1.43 dollar a year earlier.

International Business Machines (IBM), an IT company, announced third quarter adjusted EPS of 2.58 dollars, down from 2.68 dollars a year ago on revenue of 17.6 billion dollars, down from 18.0 billion dollars a year earlier. Those figures matched preliminary results released on October 8th.

Goldman Sachs (GS), the banking group, has reached an agreement with the U.S. Department of Justice to settle Malaysia's 1MDB scandal for more than 2 billion dollars, pushing its total related penalties to about 5 billion dollars, reported Bloomberg.

Moderna (MRNA), the biotechnological company, CEO Stephane Bancel said that it expects COVID-19 vaccine interim results in November, according to the Wall Street Journal.

Microsoft's (MSFT), the tech giant, price target was raised to 245 dollars from 220 dollars at Stifel.

Snap's (SNAP), the social network, price target was raised to 35 dollars from 25 dollars at Evercore.

PPG Industries (PPG), a producer of paints and coatings, reported third quarter adjusted EPS of 1.93 dollar, just above forecasts, up from 1.67 dollar a year earlier on net sales of 3.7 billion dollars, as expected, down from 3.8 billion dollars a year ago. Sales in volume declined 5%.

Cadence Design Systems (CDNS), an electronic design automation software and engineering services company, disclosed third quarter adjusted EPS of 0.70 dollar, beating estimates, up from 0.54 dollar a year ago on revenue of 666.6 million dollars, better than expected, up from 579.6 million dollars a year earlier. The company raised its full year guidance.

Later today, September housing starts (1.46 million units expected) and building permits (1.51 million units expected).

European indices are slightly bullish. The German Federal Statistical Office has posted PPI for September at +0.4% on month (vs -0.1% expected).

Asian indices closed in the red except the Chinese CSI.

WTI Crude Oil futures are posting a rebound. Later today, American Petroleum Institute (API) will release the change of U.S. oil stockpile data for October 16.

Gold and U.S dollar steady as investors await developments on U.S stimulus aid.

Gold rose 0.85 dollar (+0.04%) to 1904.93 dollars.

The dollar index fell 0.24pt to 93.188.

U.S. Equity Snapshot

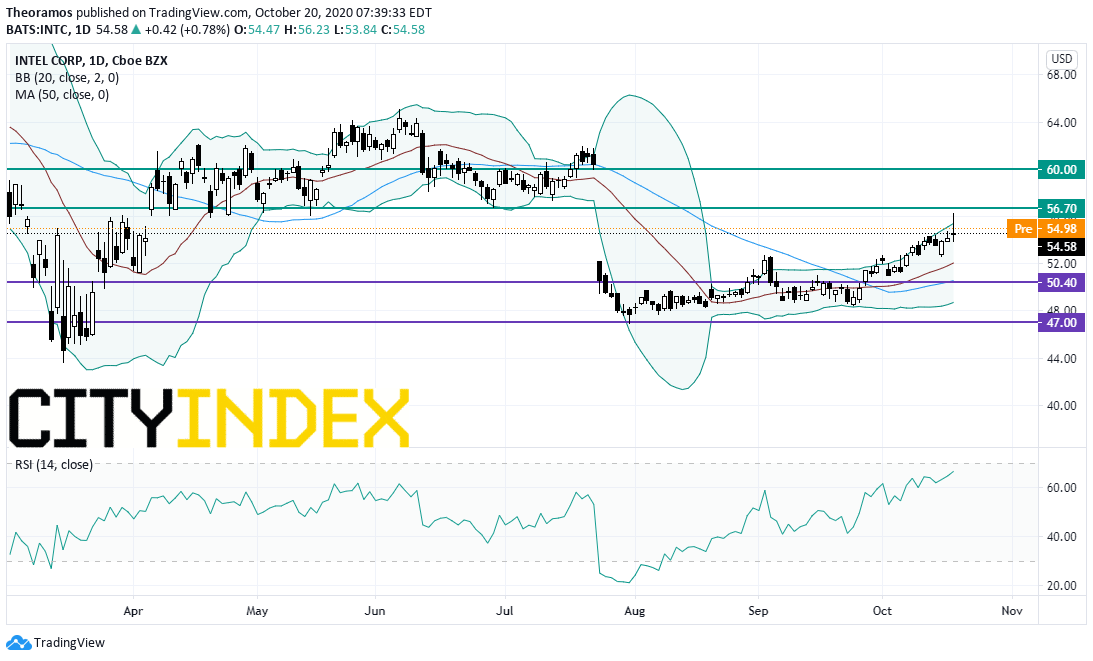

Intel (INTC), a designer and manufacturer of microprocessors, and South Korean company SK hynix "have signed an agreement under which SK hynix would acquire Intel’s NAND memory and storage business for 9 billion dollars."

Source: TradingView, GAIN Capital

Procter & Gamble (PG), a global manufacturer of consumer products, expects full year organic sales growth of 4%-5% vs a previous outlook of 2%-4% increase.

Philip Morris International (PM), a manufacturer of tobacco products, raised full year adjusted EPS guidance to 5.05-5.10 dollars from 5-5.07 dollars previously. Third quarter adjusted EPS was 1.42 dollar, beating estimates, vs 1.43 dollar a year earlier.

International Business Machines (IBM), an IT company, announced third quarter adjusted EPS of 2.58 dollars, down from 2.68 dollars a year ago on revenue of 17.6 billion dollars, down from 18.0 billion dollars a year earlier. Those figures matched preliminary results released on October 8th.

Goldman Sachs (GS), the banking group, has reached an agreement with the U.S. Department of Justice to settle Malaysia's 1MDB scandal for more than 2 billion dollars, pushing its total related penalties to about 5 billion dollars, reported Bloomberg.

Moderna (MRNA), the biotechnological company, CEO Stephane Bancel said that it expects COVID-19 vaccine interim results in November, according to the Wall Street Journal.

Microsoft's (MSFT), the tech giant, price target was raised to 245 dollars from 220 dollars at Stifel.

Snap's (SNAP), the social network, price target was raised to 35 dollars from 25 dollars at Evercore.

PPG Industries (PPG), a producer of paints and coatings, reported third quarter adjusted EPS of 1.93 dollar, just above forecasts, up from 1.67 dollar a year earlier on net sales of 3.7 billion dollars, as expected, down from 3.8 billion dollars a year ago. Sales in volume declined 5%.

Cadence Design Systems (CDNS), an electronic design automation software and engineering services company, disclosed third quarter adjusted EPS of 0.70 dollar, beating estimates, up from 0.54 dollar a year ago on revenue of 666.6 million dollars, better than expected, up from 579.6 million dollars a year earlier. The company raised its full year guidance.

Latest market news

Today 08:15 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM