EU indices slightly down | TA on Remy Cointreau

INDICES

Yesterday, European stocks were broadly lower while trading volumes were greatly reduced by a technical glitch at exchange operator Euronext. The Stoxx Europe 600 Index declined 0.18%, Germany's DAX 30 fell 0.42%, France's CAC 40 eased 0.13%, and the U.K.'s FTSE 100 was down 0.59%.

EUROPE ADVANCE/DECLINE

53% of STOXX 600 constituents traded lower or unchanged yesterday.

60% of the shares trade above their 20D MA vs 63% Friday (above the 20D moving average).

60% of the shares trade above their 200D MA vs 60% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 1.3pt to 26.62, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Industrial

3mths relative low: none

Europe Best 3 sectors

financial services, banks, real estate

Europe worst 3 sectors

chemicals, utilities, personal & household goods

INTEREST RATE

The 10yr Bund yield fell 1bp to -0.62% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -16bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Sep PPI YoY, exp.: -1.2%

GE 07:00: Sep PPI MoM, exp.: 0%

EC 09:00: Aug Current Account, exp.: E25.5B

GE 10:40: 2-Year Schatz auction, exp.: -0.73%

MORNING TRADING

On the forex front, the U.S. dollar weakened further against other major currencies, though its loss shrank at the end of the session. The ICE Dollar Index lost 0.27% to 93.43. The British pound was lifted by the European Union's comments that it was ready to intensify talks with Britain toward a trade deal. GBP/USD once breached the key 1.3000 level before closing at 1.2954, up 0.31% on day. EUR/USD jumped 0.45% to 1.1769, while USD/JPY was little changed at 105.43. AUD/USD was down for a fourth session as it dropped 0.1% to 0.7071. China's Gross Domestic Products (GDP) grew 4.9% on year in the third quarter, lower than +5.5% expected.

Meanwhile, the Chinese yuan reached a fresh 18-month high against the dollar, with USD/CNH (offshore yuan) falling 0.26% to 6.6787.

#UK - IRELAND#

BHP Group, a giant metals miner, announced that 1Q iron ore production rose 8% on year to 66 million tons and sales were up 7% to 73 million tons. The company confirmed its full-year iron ore output guidance of 244 to 253 million tons.

Next, a retailer, was upgraded to "neutral" from "sell" at Goldman Sachs.

#GERMANY#

Sartorius, a pharmaceutical and laboratory equipment supplier, reported that 9-month net income increased 37.9% on year to 211 million euros and EBITDA rose 35.3% to 489 million euros on revenue of 1.68 billion euros, up 23.9% (+25.2% at constant currency). The company said it now expects revenue growth to be at the upper end of, or slightly above, the range of 22% to 26% previously forecasted.

#FRANCE#

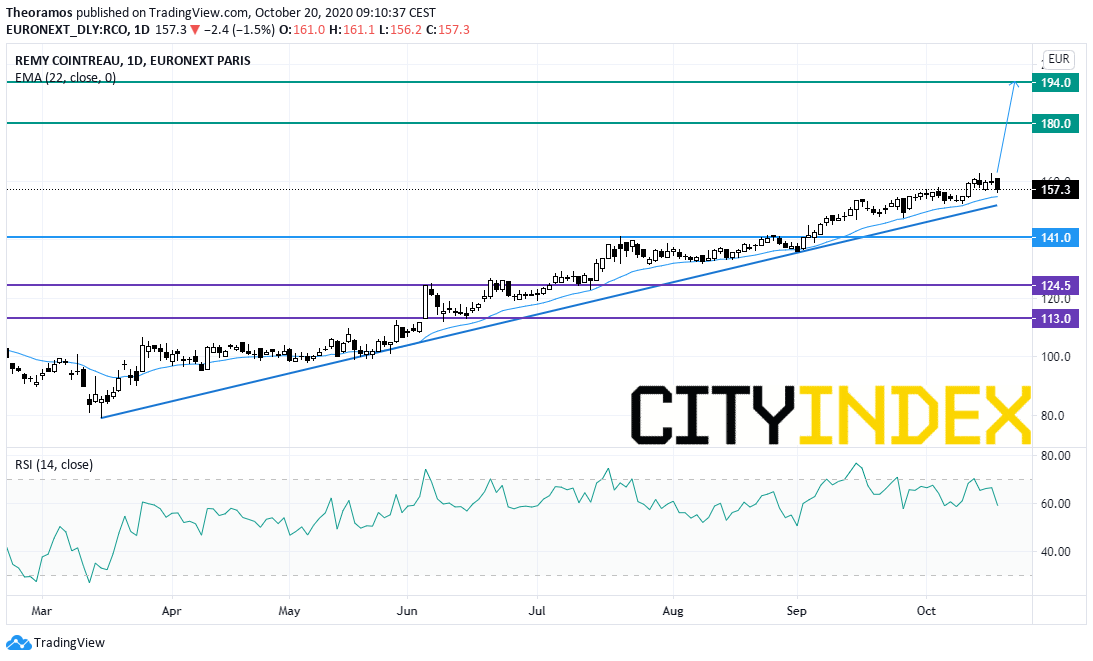

Remy Cointreau, a spirits group, announced that 1H revenue dropped 17.8% on year (-16.4% organic growth) to 431 million euros, with 2Q organic decline narrowing to 4.0% from 33.2% in 1Q. The company stated that it now expects 1H current operating profit to be down 25% - 30% on an organic basis, compared with 35% - 40% decline previously estimated.

Yesterday, European stocks were broadly lower while trading volumes were greatly reduced by a technical glitch at exchange operator Euronext. The Stoxx Europe 600 Index declined 0.18%, Germany's DAX 30 fell 0.42%, France's CAC 40 eased 0.13%, and the U.K.'s FTSE 100 was down 0.59%.

EUROPE ADVANCE/DECLINE

53% of STOXX 600 constituents traded lower or unchanged yesterday.

60% of the shares trade above their 20D MA vs 63% Friday (above the 20D moving average).

60% of the shares trade above their 200D MA vs 60% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 1.3pt to 26.62, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Industrial

3mths relative low: none

Europe Best 3 sectors

financial services, banks, real estate

Europe worst 3 sectors

chemicals, utilities, personal & household goods

INTEREST RATE

The 10yr Bund yield fell 1bp to -0.62% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -16bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Sep PPI YoY, exp.: -1.2%

GE 07:00: Sep PPI MoM, exp.: 0%

EC 09:00: Aug Current Account, exp.: E25.5B

GE 10:40: 2-Year Schatz auction, exp.: -0.73%

MORNING TRADING

On the forex front, the U.S. dollar weakened further against other major currencies, though its loss shrank at the end of the session. The ICE Dollar Index lost 0.27% to 93.43. The British pound was lifted by the European Union's comments that it was ready to intensify talks with Britain toward a trade deal. GBP/USD once breached the key 1.3000 level before closing at 1.2954, up 0.31% on day. EUR/USD jumped 0.45% to 1.1769, while USD/JPY was little changed at 105.43. AUD/USD was down for a fourth session as it dropped 0.1% to 0.7071. China's Gross Domestic Products (GDP) grew 4.9% on year in the third quarter, lower than +5.5% expected.

Meanwhile, the Chinese yuan reached a fresh 18-month high against the dollar, with USD/CNH (offshore yuan) falling 0.26% to 6.6787.

#UK - IRELAND#

BHP Group, a giant metals miner, announced that 1Q iron ore production rose 8% on year to 66 million tons and sales were up 7% to 73 million tons. The company confirmed its full-year iron ore output guidance of 244 to 253 million tons.

Next, a retailer, was upgraded to "neutral" from "sell" at Goldman Sachs.

#GERMANY#

Sartorius, a pharmaceutical and laboratory equipment supplier, reported that 9-month net income increased 37.9% on year to 211 million euros and EBITDA rose 35.3% to 489 million euros on revenue of 1.68 billion euros, up 23.9% (+25.2% at constant currency). The company said it now expects revenue growth to be at the upper end of, or slightly above, the range of 22% to 26% previously forecasted.

#FRANCE#

Remy Cointreau, a spirits group, announced that 1H revenue dropped 17.8% on year (-16.4% organic growth) to 431 million euros, with 2Q organic decline narrowing to 4.0% from 33.2% in 1Q. The company stated that it now expects 1H current operating profit to be down 25% - 30% on an organic basis, compared with 35% - 40% decline previously estimated.

From a daily point of view, the stock is supported by a rising trend line drawn since March 2020. In addition, the one-month exponential moving average plays a support role. Above 141E, targets are set at 180E and 194E in extension.

UBS Group, a banking group, announced that 3Q net income jumped to 2.09 billion dollars from 1.05 billion dollars in the prior-year period and operating income rose 26.1% on year to 8.94 billion dollars. The bank said it has established a 1.50 billion dollars capital reserve for potential share repurchases and expects buybacks to be allowed to resume in 2021.

#SWEDEN#

Swedbank, a banking group, reported that 3Q net income climbed 13% on year to 5.26 billion Swedish krona, as credit impairment reduced to 425 million Swedish krona from 1.24 billion Swedish krona in 2Q. Meanwhile, net interest income was up 2% on year to 6.71 billion Swedish krona. In addition, the bank said it is "still considering the issue of a dividend for 2019".

Source: TradingView, GAIN Capital

#SWITZERLAND#UBS Group, a banking group, announced that 3Q net income jumped to 2.09 billion dollars from 1.05 billion dollars in the prior-year period and operating income rose 26.1% on year to 8.94 billion dollars. The bank said it has established a 1.50 billion dollars capital reserve for potential share repurchases and expects buybacks to be allowed to resume in 2021.

#SWEDEN#

Swedbank, a banking group, reported that 3Q net income climbed 13% on year to 5.26 billion Swedish krona, as credit impairment reduced to 425 million Swedish krona from 1.24 billion Swedish krona in 2Q. Meanwhile, net interest income was up 2% on year to 6.71 billion Swedish krona. In addition, the bank said it is "still considering the issue of a dividend for 2019".

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM