US Futures sliding - Watch NVDA, INTC, BABA, EL, LB

The S&P 500 Futures remain under pressure after they ended in the red yesterday as Minutes from the U.S. Federal Reserve's latest meeting showed that officials expected the economy to require "additional accommodation" for recovering from the coronavirus pandemic.

Later today, investors will watch closely numbers of U.S. Initial Jobless Claims (a decline to 920,000 is expected). The Conference Board Leading Index will also be released (+1.1% on month in July expected). The Philadelphia Federal Reserve will report its Business Outlook Index for August (21.0 expected).

European indices are on the downside. The German Federal Statistical Office has posted July PPI at -1.7% (vs -1.8% on year expected).

Asian indices all closed in the red.

WTI Crude Oil futures are under pressure. The U.S. Energy Information Administration reported that U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 1.6M barrels from the previous week to 512.5M barrels for week ended August 14. U.S. crude oil inventories are about 15% above the five year average for this time of year. Standard Chartered Bank projected that September U.S. shale oil production would fall by 263K b/d to 1.65M b/d, the level of November in 2019. The bank said: "The rapid collapse in U.S. shale oil output should perhaps be the main story in the oil market; if the arrival of shale oil were an inflexion point for market perceptions, its departure should be of similar interest."

Gold and US dollar gained ground after Fed pessimistic outlook

Gold rose 1.92 dollars (+0.1%) to 1931.41 dollars while the dollar index gained 0.12pt to 93.01.

U.S. Equity Snapshot

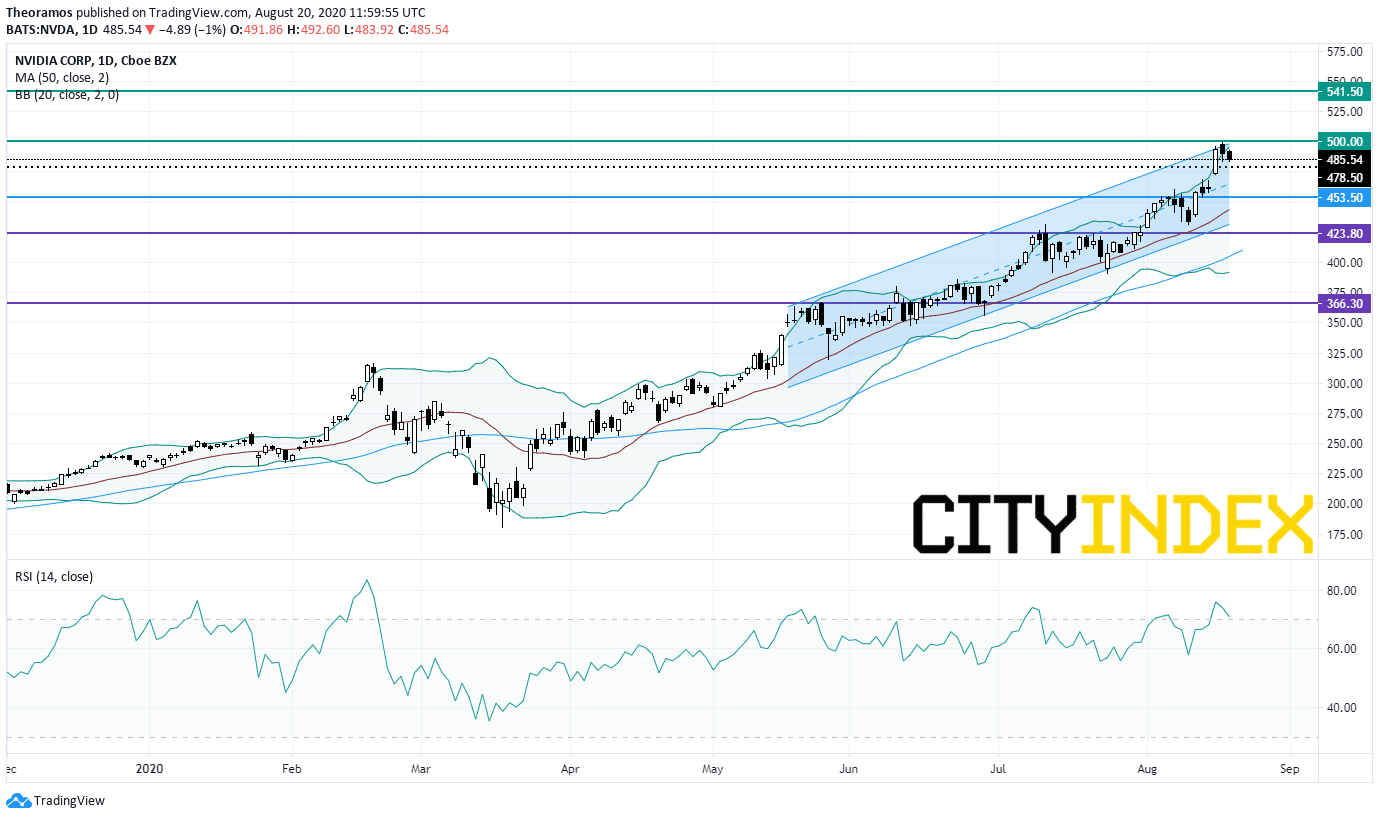

Nvidia (NVDA), a leading designer of graphics processors, released second quarter adjusted EPS and sales that beat estimates but lost some ground in extended trading, as the stock was trading to an all-time high reached on August 18 at 502.44 dollars.

Source: TradingView, GAIN Capital

Estee Lauder (EL), the cosmetics company, announced cutting 1,500 to 2,000 positions and unveiled fourth quarter and guidance that missed estimates.

L Brands (LB), a women's apparel and beauty products retailer, disclosed second quarter adjusted EPS of 0.25 dollar, significantly exceeding consensus, up from 0.24 dollar a year ago, on better than expected sales of 2.3 billion dollars, down from 2.9 billion dollars last year.

Later today, investors will watch closely numbers of U.S. Initial Jobless Claims (a decline to 920,000 is expected). The Conference Board Leading Index will also be released (+1.1% on month in July expected). The Philadelphia Federal Reserve will report its Business Outlook Index for August (21.0 expected).

European indices are on the downside. The German Federal Statistical Office has posted July PPI at -1.7% (vs -1.8% on year expected).

Asian indices all closed in the red.

WTI Crude Oil futures are under pressure. The U.S. Energy Information Administration reported that U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 1.6M barrels from the previous week to 512.5M barrels for week ended August 14. U.S. crude oil inventories are about 15% above the five year average for this time of year. Standard Chartered Bank projected that September U.S. shale oil production would fall by 263K b/d to 1.65M b/d, the level of November in 2019. The bank said: "The rapid collapse in U.S. shale oil output should perhaps be the main story in the oil market; if the arrival of shale oil were an inflexion point for market perceptions, its departure should be of similar interest."

Gold and US dollar gained ground after Fed pessimistic outlook

Gold rose 1.92 dollars (+0.1%) to 1931.41 dollars while the dollar index gained 0.12pt to 93.01.

U.S. Equity Snapshot

Nvidia (NVDA), a leading designer of graphics processors, released second quarter adjusted EPS and sales that beat estimates but lost some ground in extended trading, as the stock was trading to an all-time high reached on August 18 at 502.44 dollars.

Source: TradingView, GAIN Capital

Intel (INTC), a designer and manufacturer of microprocessors, popped after hours after announcing it is entering into accelerated share repurchase agreements to repurchase an aggregate of 10 billion dollars of the company’s common stock.

Alibaba (BABA), the Chinese online retailer, is consolidating before hours despite posting better than expected quarterly earnings.Estee Lauder (EL), the cosmetics company, announced cutting 1,500 to 2,000 positions and unveiled fourth quarter and guidance that missed estimates.

L Brands (LB), a women's apparel and beauty products retailer, disclosed second quarter adjusted EPS of 0.25 dollar, significantly exceeding consensus, up from 0.24 dollar a year ago, on better than expected sales of 2.3 billion dollars, down from 2.9 billion dollars last year.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM