U.S Futures red – Watch NVDA, COTY, LB, JPM, JACK, KEYS

The S&P 500 Futures remain on the downside after they gave up earlier gains yesterday to close at session lows. Market sentiment was dampened by New York City's decision to close public school indefinitely in view of increasing coronavirus cases.

Later today, the U.S. Labor Department will post initial jobless claims in the week ending November 14 (0.7 million expected). The Philadelphia Federal Reserve will report its Business Outlook Index for November (22.5). The Conference Board will post its Leading Index for October (+0.7% on month expected). The National Association of Realtors will report October existing home sales (6.46 million units expected).

European indices are on the downside. September Eurozone Output was released at -2.9% on month, vs +2.6% expected.

Asian indices closed in dispersed order as the Japanese Nikkei and Hong Kong HSI were down when the Chinese CSI and the Australian ASX ended in the green. Official data showed that the Australian economy added 178,800 jobs in October (-27,500 jobs expected), while jobless rate edged up to 7.0% (7.1% expected) from 6.9% in September.

WTI Crude Oil is turning down. The U.S. Energy Information Administration (EIA) reported that U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 0.8M barrels from the previous week to 489.5M barrels for week ending November 13. Besides, U.S. crude oil production increased to 10.9M b/d from 10.5M b/d.

U.S indices closed down on Wednesday, pressured by Energy (-2.88%), Utilities (-1.94%) and Pharmaceuticals, Biotechnology & Life Sciences (-1.79%) sectors.

Approximately 90% of stocks in the S&P 500 Index were trading above their 200-day moving average and 85% were trading above their 20-day moving average. The VIX Index jumped 1.13pt (+4.98%) to 23.84 and WTI Crude Oil rose $0.21 (+0.51%) to $41.64 at the close.

On the U.S economic data front, the Mortgage Bankers Association's Mortgage Applications declined 0.3% for the week ending November 13th compared to -0.5% in the previous week. Finally, Housing Starts spiked to 1,530K on month in October (1,460K expected), from a revised 1,459K in September.

Gold lost some ground on firmer U.S dollar and positive COVID-19 vaccine news.

Gold fell 8.36 dollars (-0.45%) to 1863.87 dollars.

The dollar index rose 0.22pt to 92.537.

U.S. Equity Snapshot

Source: TradingView, GAIN Capital

Coty (COTY), the global beauty company, was upgraded to "buy" from "neutral" at Citigroup.

L Brands (LB), a women's apparel and beauty products retailer, announced third quarter adjusted EPS of 1.13 dollar, significantly above the consensus, up from 0.02 dollar a year ago on sales of 3.1 billion dollars, also above estimates, up from 2.7 billion dollars a year earlier.

JPMorgan (JPM), the banking group, was downgraded to "market perform" from "outperform" at KBW.

Jack in the Box (JACK), the restaurant company, surged after posting fourth quarter earnings that beat estimates.

Keysight Technologies (KEYS), a provider of electronic measurement devices and software solutions, disclosed fourth quarter adjusted EPS of 1.62 dollar, beating estimates, up from 1.33 dollar a year ago on revenue of 1.2 billion dollars, as expected, up from 1.1 billion dollars a year earlier. The company unveiled first quarter adjusted EPS forecast that also exceeded estimates.

Later today, the U.S. Labor Department will post initial jobless claims in the week ending November 14 (0.7 million expected). The Philadelphia Federal Reserve will report its Business Outlook Index for November (22.5). The Conference Board will post its Leading Index for October (+0.7% on month expected). The National Association of Realtors will report October existing home sales (6.46 million units expected).

European indices are on the downside. September Eurozone Output was released at -2.9% on month, vs +2.6% expected.

Asian indices closed in dispersed order as the Japanese Nikkei and Hong Kong HSI were down when the Chinese CSI and the Australian ASX ended in the green. Official data showed that the Australian economy added 178,800 jobs in October (-27,500 jobs expected), while jobless rate edged up to 7.0% (7.1% expected) from 6.9% in September.

WTI Crude Oil is turning down. The U.S. Energy Information Administration (EIA) reported that U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 0.8M barrels from the previous week to 489.5M barrels for week ending November 13. Besides, U.S. crude oil production increased to 10.9M b/d from 10.5M b/d.

U.S indices closed down on Wednesday, pressured by Energy (-2.88%), Utilities (-1.94%) and Pharmaceuticals, Biotechnology & Life Sciences (-1.79%) sectors.

Approximately 90% of stocks in the S&P 500 Index were trading above their 200-day moving average and 85% were trading above their 20-day moving average. The VIX Index jumped 1.13pt (+4.98%) to 23.84 and WTI Crude Oil rose $0.21 (+0.51%) to $41.64 at the close.

On the U.S economic data front, the Mortgage Bankers Association's Mortgage Applications declined 0.3% for the week ending November 13th compared to -0.5% in the previous week. Finally, Housing Starts spiked to 1,530K on month in October (1,460K expected), from a revised 1,459K in September.

Gold lost some ground on firmer U.S dollar and positive COVID-19 vaccine news.

Gold fell 8.36 dollars (-0.45%) to 1863.87 dollars.

The dollar index rose 0.22pt to 92.537.

U.S. Equity Snapshot

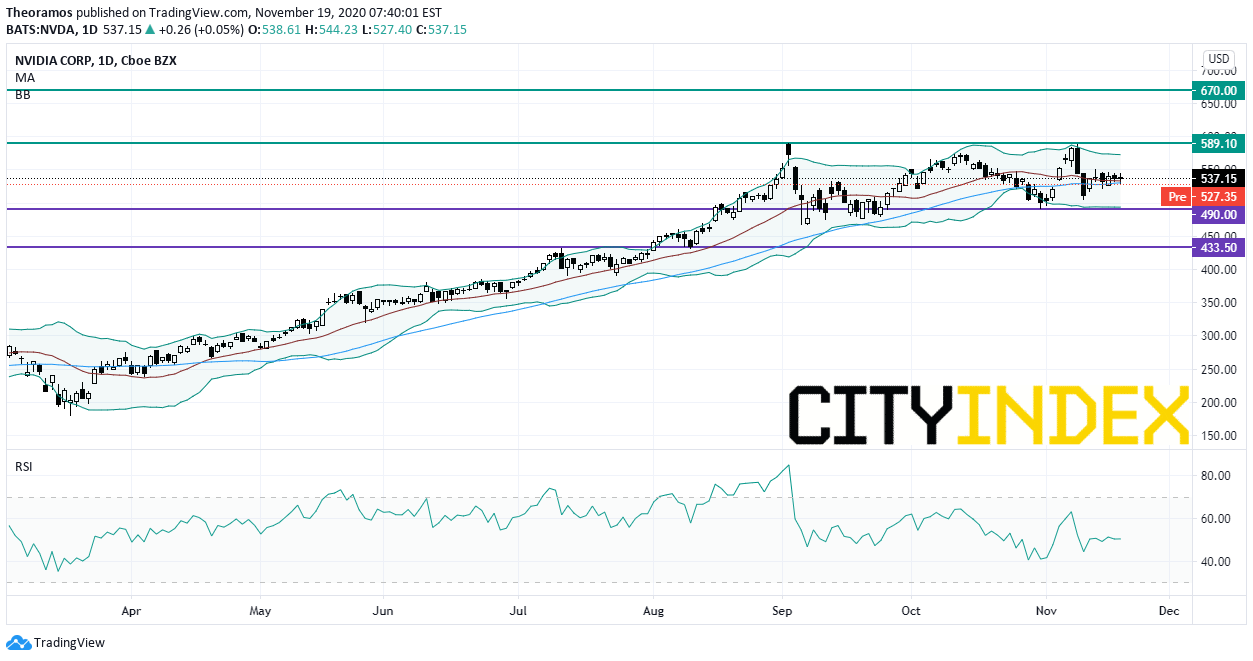

Nvidia (NVDA), a leading designer of graphics processors, lost ground postmarket as the company's CFO warned that data center chip sales are likely to fall slightly during the current quarter. Separately, the company posted third quarter earnings that beat estimates.

Source: TradingView, GAIN Capital

Coty (COTY), the global beauty company, was upgraded to "buy" from "neutral" at Citigroup.

L Brands (LB), a women's apparel and beauty products retailer, announced third quarter adjusted EPS of 1.13 dollar, significantly above the consensus, up from 0.02 dollar a year ago on sales of 3.1 billion dollars, also above estimates, up from 2.7 billion dollars a year earlier.

JPMorgan (JPM), the banking group, was downgraded to "market perform" from "outperform" at KBW.

Jack in the Box (JACK), the restaurant company, surged after posting fourth quarter earnings that beat estimates.

Keysight Technologies (KEYS), a provider of electronic measurement devices and software solutions, disclosed fourth quarter adjusted EPS of 1.62 dollar, beating estimates, up from 1.33 dollar a year ago on revenue of 1.2 billion dollars, as expected, up from 1.1 billion dollars a year earlier. The company unveiled first quarter adjusted EPS forecast that also exceeded estimates.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM