EU indices slightly up | TA focus on GN Store Nord

INDICES

Yesterday, European stocks were broadly lower. The Stoxx Europe 600 Index dropped 0.56%. Germany's DAX 30 slipped 0.30%, France's CAC 40 lost 0.68%, and the U.K.'s FTSE 100 was down 0.83%.

EUROPE ADVANCE/DECLINE

77% of STOXX 600 constituents traded lower or unchanged yesterday.

55% of the shares trade above their 20D MA vs 65% Monday (above the 20D moving average).

51% of the shares trade above their 200D MA vs 54% Monday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 0.49pt to 23.27, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Retail

3mths relative low: none

Europe Best 3 sectors

insurance, personal & household goods, retail

Europe worst 3 sectors

real estate, utilities, energy

INTEREST RATE

The 10yr Bund yield fell 3bps to -0.45% (above its 20D MA). The 2yr-10yr yield spread rose 1bp to -19bps (below its 20D MA).

ECONOMIC DATA

UK : UK-EU Brexit Talks

UK 07:00: Jul Retail Price Idx MoM, exp.: 0.2%

UK 07:00: Jul Retail Price Idx YoY, exp.: 1.1%

UK 07:00: Jul PPI Core Output YoY, exp.: 0.5%

UK 07:00: Jul PPI Core Output MoM, exp.: 0%

UK 07:00: Jul PPI Output YoY, exp.: -0.8%

UK 07:00: Jul PPI Input MoM, exp.: 2.4%

UK 07:00: Jul PPI Input YoY, exp.: -6.4%

UK 07:00: Jul PPI Output MoM, exp.: 0.3%

UK 07:00: Jul Core Inflation Rate YoY, exp.: 1.4%

UK 07:00: Jul Inflation Rate MoM, exp.: 0.1%

UK 07:00: Jul Inflation Rate YoY, exp.: 0.6%

UK 07:00: Jul Core Inflation Rate MoM, exp.: 0.2%

EC 09:00: Jun Current Account, exp.: E-10.5B

EC 10:00: Jul Core Inflation Rate YoY final, exp.: 0.8%

EC 10:00: Jul Inflation Rate MoM final, exp.: 0.3%

EC 10:00: Jul Inflation Rate YoY final, exp.: 0.3%

GE 10:40: 30-Year Bund auction, exp.: -0.06%

MORNING TRADING

In Asian trading hours, EUR/USD held gains at 1.1937 and GBP/USD was firm at 1.3244. USD/JPY remains subdued at 105.39. This morning, official data showed that Japan's exports declined 19.2% on year in July (-20.9% expected), while core machine orders dropped 7.6% on month in June (+2.0% expected).

Spot gold dropped to $1,994 an ounce.

#UK - IRELAND#

Softcat, an IT infrastructure provider, posted a full-year trading update: "Following the third quarter update provided in May, the Company has continued to trade satisfactorily during the final three months of the year and has delivered operating profit for the full year slightly ahead of the Board's expectations. Cash generation also remained strong and it is now the Company's intention to resume its normal dividend policy and timetable later this year. This will include payment of the interim dividend previously cancelled in March of this year."

Rio Tinto, a giant miner, has lowered its full-year refined copper production guidance to 135k - 175k tons from 165k - 205k tons previously, saying its "Kennecott mine in Utah has experienced delays to the restart of the smelter due to unexpected issues that appeared following planned maintenance."

#GERMANY#

RWE, an electric utilities company, said it has raised 2 billion euros from share issue to support its renewable energy expansion, including a 480 million dollars acquisition of the 2.7 GW project pipeline from Nordex as announced on July 31.

#BENELUX#

Galapagos, a pharmaceutical research company, reported that the U.S. Food and Drug Administration has requested data before completing its review of the New Drug Application for filgotinib, and "has expressed concerns regarding the overall benefit/risk profile of the filgotinib 200 mg dose".

#SWITZERLAND#

Alcon, an eye care company, posted 2Q core LPS of 0.21 dollar, compared with a core EPS of 0.47 dollar in the prior-year period, and net sales declined 36% on year (-34% at constant currency) to 1.20 billion dollars. The company said: "Due to the uncertain scope and duration of the ongoing COVID-19 outbreak, the Company is unable to provide an estimate for financial results for the full year 2020."

Clariant, a speciality chemicals company, was downgraded to "equalweight" from "overweight" at Barclays.

#DENMARK#

Maersk, a Danish integrated shipping company, announced that 2Q underlying profit from continuing operations jumped to 359 million dollars from 134 million dollars in the prior-year period, and EBITDA rose 25.1% on year to 1.70 billion dollars on revenue of 9.00 billion dollars, down 6.5%. The company said: " The continued improvement in operating results were driven by strong cost performance across all of our businesses, lower fuel prices and higher freight rates on Ocean and increased profitability in Logistics & Services. (...) Reinstating full-year guidance for 2020 with EBITDA expectations between USD 6.0bn-7.0bn compared to the initial full-year guidance of an EBITDA around USD 5.5bn."

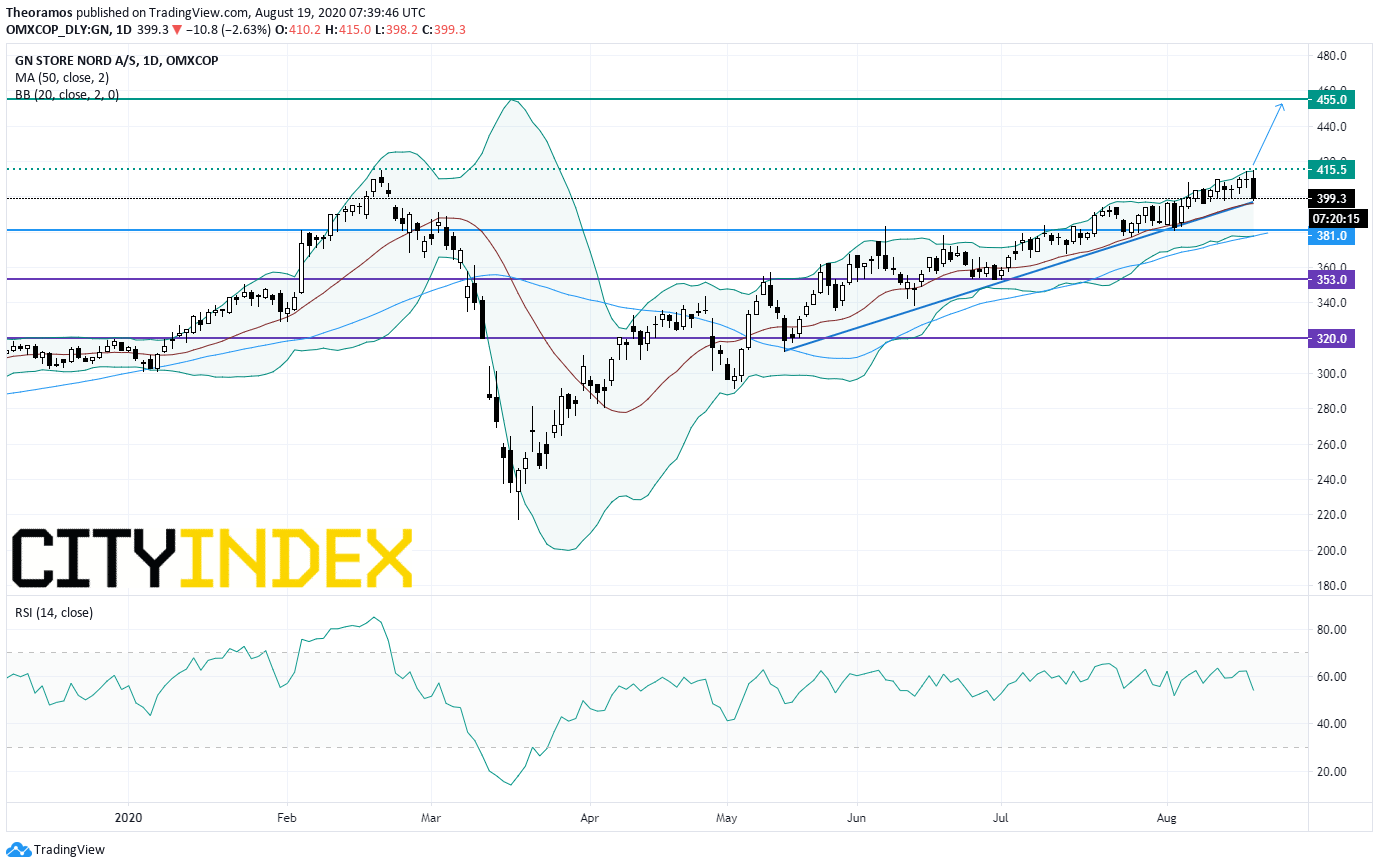

GN Store Nord, a Danish manufacturer of hearing aids and headsets, reported that 2Q EPS declined 97% on year to 0.06 Danish krone and EBITA dropped 95% to 25 million Danish krone on revenue of 2.66 billion Danish krone, down 13%. The company said it was COVID-19 caused "ripple effects of production shutdown in Q1" and "various demand implications as consumers stayed at home, and as enterprises continued to invest in employees working from home".

From a daily point of view, the stock is supported by a rising trend line drawn since May. Furthermore, the 20DMA is playing the role of support. A break above the previous all-time high of February at 415.5DKK would trigger a new up leg with a target set at 455DKK.

Source: GAIN Capital, TradingView

Yesterday, European stocks were broadly lower. The Stoxx Europe 600 Index dropped 0.56%. Germany's DAX 30 slipped 0.30%, France's CAC 40 lost 0.68%, and the U.K.'s FTSE 100 was down 0.83%.

EUROPE ADVANCE/DECLINE

77% of STOXX 600 constituents traded lower or unchanged yesterday.

55% of the shares trade above their 20D MA vs 65% Monday (above the 20D moving average).

51% of the shares trade above their 200D MA vs 54% Monday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 0.49pt to 23.27, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Retail

3mths relative low: none

Europe Best 3 sectors

insurance, personal & household goods, retail

Europe worst 3 sectors

real estate, utilities, energy

INTEREST RATE

The 10yr Bund yield fell 3bps to -0.45% (above its 20D MA). The 2yr-10yr yield spread rose 1bp to -19bps (below its 20D MA).

ECONOMIC DATA

UK : UK-EU Brexit Talks

UK 07:00: Jul Retail Price Idx MoM, exp.: 0.2%

UK 07:00: Jul Retail Price Idx YoY, exp.: 1.1%

UK 07:00: Jul PPI Core Output YoY, exp.: 0.5%

UK 07:00: Jul PPI Core Output MoM, exp.: 0%

UK 07:00: Jul PPI Output YoY, exp.: -0.8%

UK 07:00: Jul PPI Input MoM, exp.: 2.4%

UK 07:00: Jul PPI Input YoY, exp.: -6.4%

UK 07:00: Jul PPI Output MoM, exp.: 0.3%

UK 07:00: Jul Core Inflation Rate YoY, exp.: 1.4%

UK 07:00: Jul Inflation Rate MoM, exp.: 0.1%

UK 07:00: Jul Inflation Rate YoY, exp.: 0.6%

UK 07:00: Jul Core Inflation Rate MoM, exp.: 0.2%

EC 09:00: Jun Current Account, exp.: E-10.5B

EC 10:00: Jul Core Inflation Rate YoY final, exp.: 0.8%

EC 10:00: Jul Inflation Rate MoM final, exp.: 0.3%

EC 10:00: Jul Inflation Rate YoY final, exp.: 0.3%

GE 10:40: 30-Year Bund auction, exp.: -0.06%

MORNING TRADING

In Asian trading hours, EUR/USD held gains at 1.1937 and GBP/USD was firm at 1.3244. USD/JPY remains subdued at 105.39. This morning, official data showed that Japan's exports declined 19.2% on year in July (-20.9% expected), while core machine orders dropped 7.6% on month in June (+2.0% expected).

Spot gold dropped to $1,994 an ounce.

#UK - IRELAND#

Softcat, an IT infrastructure provider, posted a full-year trading update: "Following the third quarter update provided in May, the Company has continued to trade satisfactorily during the final three months of the year and has delivered operating profit for the full year slightly ahead of the Board's expectations. Cash generation also remained strong and it is now the Company's intention to resume its normal dividend policy and timetable later this year. This will include payment of the interim dividend previously cancelled in March of this year."

Rio Tinto, a giant miner, has lowered its full-year refined copper production guidance to 135k - 175k tons from 165k - 205k tons previously, saying its "Kennecott mine in Utah has experienced delays to the restart of the smelter due to unexpected issues that appeared following planned maintenance."

#GERMANY#

RWE, an electric utilities company, said it has raised 2 billion euros from share issue to support its renewable energy expansion, including a 480 million dollars acquisition of the 2.7 GW project pipeline from Nordex as announced on July 31.

#BENELUX#

Galapagos, a pharmaceutical research company, reported that the U.S. Food and Drug Administration has requested data before completing its review of the New Drug Application for filgotinib, and "has expressed concerns regarding the overall benefit/risk profile of the filgotinib 200 mg dose".

#SWITZERLAND#

Alcon, an eye care company, posted 2Q core LPS of 0.21 dollar, compared with a core EPS of 0.47 dollar in the prior-year period, and net sales declined 36% on year (-34% at constant currency) to 1.20 billion dollars. The company said: "Due to the uncertain scope and duration of the ongoing COVID-19 outbreak, the Company is unable to provide an estimate for financial results for the full year 2020."

Clariant, a speciality chemicals company, was downgraded to "equalweight" from "overweight" at Barclays.

#DENMARK#

Maersk, a Danish integrated shipping company, announced that 2Q underlying profit from continuing operations jumped to 359 million dollars from 134 million dollars in the prior-year period, and EBITDA rose 25.1% on year to 1.70 billion dollars on revenue of 9.00 billion dollars, down 6.5%. The company said: " The continued improvement in operating results were driven by strong cost performance across all of our businesses, lower fuel prices and higher freight rates on Ocean and increased profitability in Logistics & Services. (...) Reinstating full-year guidance for 2020 with EBITDA expectations between USD 6.0bn-7.0bn compared to the initial full-year guidance of an EBITDA around USD 5.5bn."

GN Store Nord, a Danish manufacturer of hearing aids and headsets, reported that 2Q EPS declined 97% on year to 0.06 Danish krone and EBITA dropped 95% to 25 million Danish krone on revenue of 2.66 billion Danish krone, down 13%. The company said it was COVID-19 caused "ripple effects of production shutdown in Q1" and "various demand implications as consumers stayed at home, and as enterprises continued to invest in employees working from home".

From a daily point of view, the stock is supported by a rising trend line drawn since May. Furthermore, the 20DMA is playing the role of support. A break above the previous all-time high of February at 415.5DKK would trigger a new up leg with a target set at 455DKK.

Source: GAIN Capital, TradingView

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Commodities articles

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM

April 14, 2024 11:37 PM