EU indices down this morning | TA focus on Next

INDICES

Yesterday, European stocks were broadly higher. The Stoxx Europe 600 Index advanced 0.58%, Germany's DAX 30 gained 0.29%, France's CAC 40 edged up 0.13%, while the U.K.'s FTSE 100 retreated 0.44%.

EUROPE ADVANCE/DECLINE

64% of STOXX 600 constituents traded higher yesterday.

63% of the shares trade above their 20D MA vs 59% Tuesday (above the 20D moving average).

59% of the shares trade above their 200D MA vs 58% Tuesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 0.12pt to 21.99, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Retail, Industrial, Basic Resources

3mths relative low: Telecom., Banks, Utilities

Europe Best 3 sectors

basic resources, real estate, retail

Europe worst 3 sectors

automobiles & parts, utilities, health care

INTEREST RATE

The 10yr Bund yield was unchanged to -0.48% (below its 20D MA). The 2yr-10yr yield spread rose 0bp to -21bps (above its 20D MA).

ECONOMIC DATA

EC 09:00: ECB Guindos speech

EC 10:00: Aug Inflation Rate MoM final, exp.: -0.4%

EC 10:00: Aug Core Inflation Rate YoY final, exp.: 1.2%

EC 10:00: Aug Inflation Rate YoY final, exp.: 0.4%

EC 10:00: Jul Construction Output YoY, exp.: -5.9%

FR 10:00: 3-Year BTAN auction, exp.: -0.58%

FR 10:00: 5-Year BTAN auction, exp.: -0.45%

UK 12:00: BoE Interest Rate Decision, exp.: 0.1%

UK 12:00: BoE Quantitative Easing, exp.: £745B

UK 12:00: MPC Meeting Minutes

UK 12:00: BoE MPC Vote Hike, exp.: 0/9

UK 12:00: BoE MPC Vote Unchanged, exp.: 44083

UK 12:00: BoE MPC Vote Cut, exp.: 0/9

MORNING TRADING

In Asian trading hours, the U.S. dollar gained strength, as EUR/USD dropped further to 1.1766 and GBP/USD retreated to 1.2927. USD/JPY held above the 105.00 level. The Bank of Japan kept its benchmark rate at -0.10% as expected. AUD/USD fell to 0.7278. Official data showed that the Australian economy added 111,000 jobs in August (-35,000 jobs expected), while jobless rate dropped to 6.8% (7.7% expected) from 7.5% in July.

Spot gold slid to $1,947 an ounce.

#UK - IRELAND#

Next, a retail group, released 1H results: "Brand full price sales in the first half of this year were down -33% on last year and total sales (including markdown sales) were down -34%. Profit before tax in the first half of the year was £9m (on a pre-IFRS 16 basis) and we reduced our net debt by £347m to £765m. Full price sales at the beginning of the second half have continued to exceed our expectations and we have revised our central scenario for full year profit, up from £195m to £300m."

Source: GAIN Capital, TradingView

Playtech, a gambling software development company, reported that 1H adjusted EPS from continuing operations declined 37% on year to 0.144 euro and adjusted EBITDA dropped 16% to 162 million euros on revenue of 564 million euros, down 23% (-22% at constant currency).

Informa, a business intelligence company, was downgraded to "neutral" from "overweight" at JPMorgan.

Segro, a property group, was upgraded to "buy" from "hold" at HSBC.

Compass Group, a contract foodservice company, was upgraded to "overweight" from "equalweight" at Barclays.

#GERMANY#

HeidelbergCement, a building materials company, was upgraded to "equalweight" from "underweight" at Barclays.

RWE, an electric utilities company, was downgraded to "hold" from "buy" at Societe Generale.

#FRANCE#

Euronext, a stock exchange operator, was downgraded to "hold" from "buy" at HSBC.

#SPAIN#

CaixaBank and Bankia, the two Spanish banks, were upgraded to "buy" from "hold" at HSBC.

#BENELUX#

Unibail-Rodamco-Westfield, a commercial real estate company, announced a 9 billion euros deleveraging plan to strengthen its balance sheet, including a fully underwritten 3.5 billion euros capital raise to be used to immediately reduce leverage, 1.0 billion euros cash savings over the next two years by limiting cash dividends, a further 0.8 billion reduction in operating capex and 4.0 billion euros of disposals expected to be completed by year-end 2021.

EX-DIVIDEND

Intertek Group:34.2p

Yesterday, European stocks were broadly higher. The Stoxx Europe 600 Index advanced 0.58%, Germany's DAX 30 gained 0.29%, France's CAC 40 edged up 0.13%, while the U.K.'s FTSE 100 retreated 0.44%.

EUROPE ADVANCE/DECLINE

64% of STOXX 600 constituents traded higher yesterday.

63% of the shares trade above their 20D MA vs 59% Tuesday (above the 20D moving average).

59% of the shares trade above their 200D MA vs 58% Tuesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 0.12pt to 21.99, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Retail, Industrial, Basic Resources

3mths relative low: Telecom., Banks, Utilities

Europe Best 3 sectors

basic resources, real estate, retail

Europe worst 3 sectors

automobiles & parts, utilities, health care

INTEREST RATE

The 10yr Bund yield was unchanged to -0.48% (below its 20D MA). The 2yr-10yr yield spread rose 0bp to -21bps (above its 20D MA).

ECONOMIC DATA

EC 09:00: ECB Guindos speech

EC 10:00: Aug Inflation Rate MoM final, exp.: -0.4%

EC 10:00: Aug Core Inflation Rate YoY final, exp.: 1.2%

EC 10:00: Aug Inflation Rate YoY final, exp.: 0.4%

EC 10:00: Jul Construction Output YoY, exp.: -5.9%

FR 10:00: 3-Year BTAN auction, exp.: -0.58%

FR 10:00: 5-Year BTAN auction, exp.: -0.45%

UK 12:00: BoE Interest Rate Decision, exp.: 0.1%

UK 12:00: BoE Quantitative Easing, exp.: £745B

UK 12:00: MPC Meeting Minutes

UK 12:00: BoE MPC Vote Hike, exp.: 0/9

UK 12:00: BoE MPC Vote Unchanged, exp.: 44083

UK 12:00: BoE MPC Vote Cut, exp.: 0/9

MORNING TRADING

In Asian trading hours, the U.S. dollar gained strength, as EUR/USD dropped further to 1.1766 and GBP/USD retreated to 1.2927. USD/JPY held above the 105.00 level. The Bank of Japan kept its benchmark rate at -0.10% as expected. AUD/USD fell to 0.7278. Official data showed that the Australian economy added 111,000 jobs in August (-35,000 jobs expected), while jobless rate dropped to 6.8% (7.7% expected) from 7.5% in July.

Spot gold slid to $1,947 an ounce.

#UK - IRELAND#

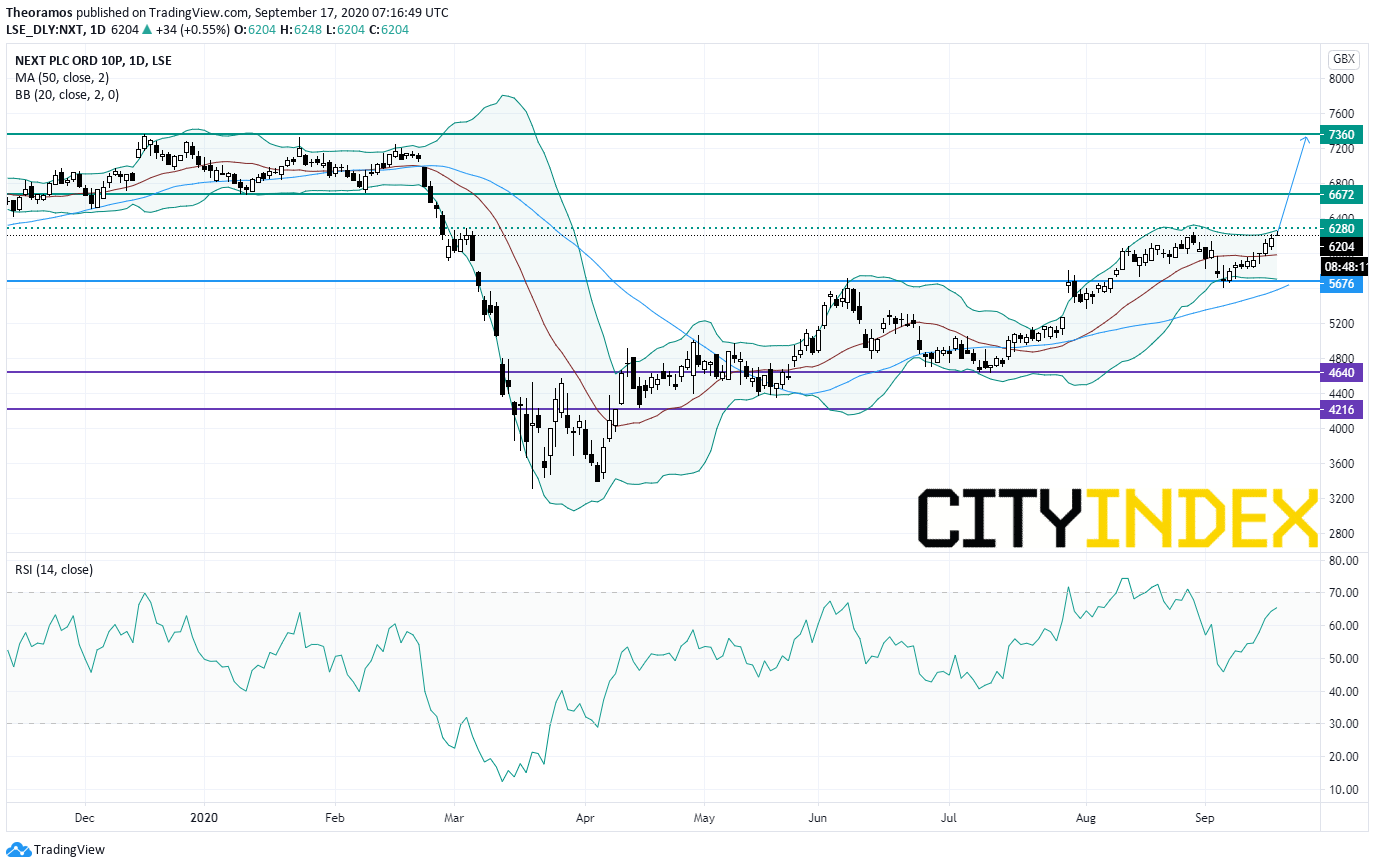

Next, a retail group, released 1H results: "Brand full price sales in the first half of this year were down -33% on last year and total sales (including markdown sales) were down -34%. Profit before tax in the first half of the year was £9m (on a pre-IFRS 16 basis) and we reduced our net debt by £347m to £765m. Full price sales at the beginning of the second half have continued to exceed our expectations and we have revised our central scenario for full year profit, up from £195m to £300m."

From a chartist point of view, the stock is testing the horizontal resistance of March 2020at 6280p. Moreover, the Relative Strength Index (RSI, 14) is bouncing. Above 5600p (overlap area around 5676p), look for 6672p and the previous top of December 2019 at 7360p in extension.

Source: GAIN Capital, TradingView

Playtech, a gambling software development company, reported that 1H adjusted EPS from continuing operations declined 37% on year to 0.144 euro and adjusted EBITDA dropped 16% to 162 million euros on revenue of 564 million euros, down 23% (-22% at constant currency).

Informa, a business intelligence company, was downgraded to "neutral" from "overweight" at JPMorgan.

Segro, a property group, was upgraded to "buy" from "hold" at HSBC.

Compass Group, a contract foodservice company, was upgraded to "overweight" from "equalweight" at Barclays.

#GERMANY#

HeidelbergCement, a building materials company, was upgraded to "equalweight" from "underweight" at Barclays.

RWE, an electric utilities company, was downgraded to "hold" from "buy" at Societe Generale.

#FRANCE#

Euronext, a stock exchange operator, was downgraded to "hold" from "buy" at HSBC.

#SPAIN#

CaixaBank and Bankia, the two Spanish banks, were upgraded to "buy" from "hold" at HSBC.

#BENELUX#

Unibail-Rodamco-Westfield, a commercial real estate company, announced a 9 billion euros deleveraging plan to strengthen its balance sheet, including a fully underwritten 3.5 billion euros capital raise to be used to immediately reduce leverage, 1.0 billion euros cash savings over the next two years by limiting cash dividends, a further 0.8 billion reduction in operating capex and 4.0 billion euros of disposals expected to be completed by year-end 2021.

EX-DIVIDEND

Intertek Group:34.2p

Latest market news

Latest Commodities articles

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM

April 14, 2024 11:37 PM