US Futures consolidating - Watch BAC, MS, AAL, DELL, AA

The S&P 500 Futures are facing a consolidation after they advanced further yesterday.

Later today, the U.S. Commerce Department will release June retail sales (+5.0% on month expected) and May business inventories (-2.3% on month expected). The Labor Department will report initial jobless claims in the week ended July 11 (1.25 million expected). The Philadelphia Federal Reserve will post its Business Outlook Index for July (20.0 expected). The National Association of Home Builders will release Housing Market Index for July (61 expected).

European indices are still navigating choppy waters. The European Central Bank has announced its interest rates decision, let unchanged as expected. ECB also decided to keep pandemic bond-buying program unchanged at 1.35 trillion euros. The European Commission has reported May trade balance at 9.4 billion euros (vs 1.6 billion euros surplus in April). France's INSEE has posted final readings of June CPI at +0.2% (vs +0.1% on year expected). The U.K. Office for National Statistics has reported ILO jobless rate for the three months to May at 3.9% (vs 4.2% expected).

Asian indices all closed in the red. This morning, official data showed that China's 2Q GDP grew 3.2% on year (+2.4% expected) and China's industrial production rose 4.8% in June (as expected), while retail sales declined 1.8% (+0.5% expected). On the other hand, the Australian economy added 210,800 jobs in June (+100,000 jobs expected), though full-time jobs dropped 38,100 while part-time jobs increased 249,000, according to the government. Also, Australia's jobless rate climbed to 7.4% in June (7.2% expected) from 7.1% in May.

WTI Crude Oil futures are facing a consolidation. The U.S. Energy Information Administration reported a surprise reduction of 7.49 million barrels in crude-oil stockpiles last week, in contrast to an addition of 250,000 barrels expected.

Gold declined 2.77 dollars (-0.15%) to 1807.52 dollars.

USD is posting a rebound on renewed tensions between the U.S. and China.

EUR/USD declined 19pips to 1.1393 the day's range was 1.1386 - 1.1419 compared to 1.1391 - 1.1452 the previous session.

U.S. Equity Snapshot

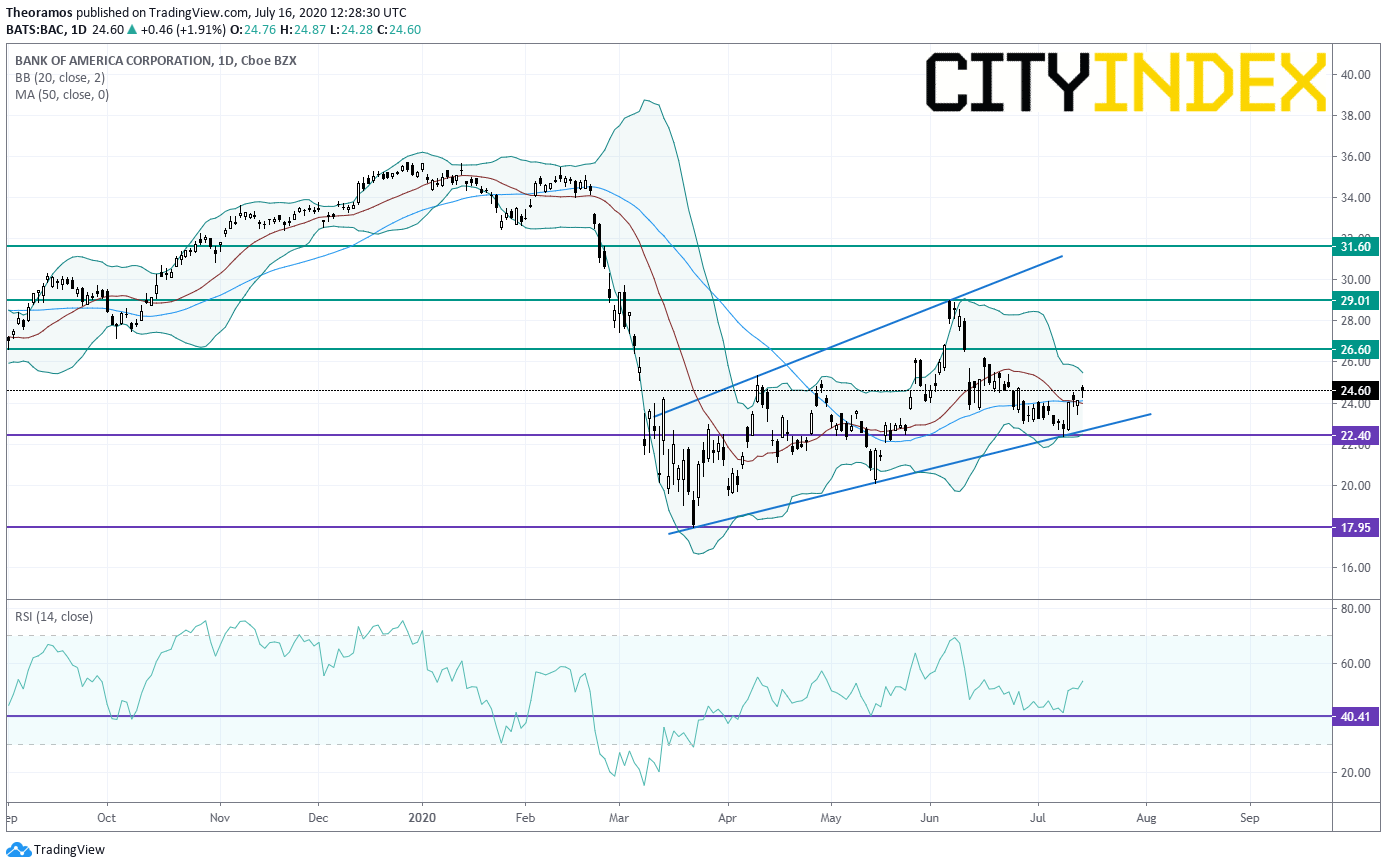

Bank of America (BAC), the financial institution, is under pressure before hours after reporting second quarter EPS down 52% to 0.37 dollar, above estimates, from 0.74 dollar a year earlier. Net revenue declined 3% to 22.33 billion dollars.

Later today, the U.S. Commerce Department will release June retail sales (+5.0% on month expected) and May business inventories (-2.3% on month expected). The Labor Department will report initial jobless claims in the week ended July 11 (1.25 million expected). The Philadelphia Federal Reserve will post its Business Outlook Index for July (20.0 expected). The National Association of Home Builders will release Housing Market Index for July (61 expected).

European indices are still navigating choppy waters. The European Central Bank has announced its interest rates decision, let unchanged as expected. ECB also decided to keep pandemic bond-buying program unchanged at 1.35 trillion euros. The European Commission has reported May trade balance at 9.4 billion euros (vs 1.6 billion euros surplus in April). France's INSEE has posted final readings of June CPI at +0.2% (vs +0.1% on year expected). The U.K. Office for National Statistics has reported ILO jobless rate for the three months to May at 3.9% (vs 4.2% expected).

Asian indices all closed in the red. This morning, official data showed that China's 2Q GDP grew 3.2% on year (+2.4% expected) and China's industrial production rose 4.8% in June (as expected), while retail sales declined 1.8% (+0.5% expected). On the other hand, the Australian economy added 210,800 jobs in June (+100,000 jobs expected), though full-time jobs dropped 38,100 while part-time jobs increased 249,000, according to the government. Also, Australia's jobless rate climbed to 7.4% in June (7.2% expected) from 7.1% in May.

WTI Crude Oil futures are facing a consolidation. The U.S. Energy Information Administration reported a surprise reduction of 7.49 million barrels in crude-oil stockpiles last week, in contrast to an addition of 250,000 barrels expected.

Gold declined 2.77 dollars (-0.15%) to 1807.52 dollars.

USD is posting a rebound on renewed tensions between the U.S. and China.

EUR/USD declined 19pips to 1.1393 the day's range was 1.1386 - 1.1419 compared to 1.1391 - 1.1452 the previous session.

U.S. Equity Snapshot

Bank of America (BAC), the financial institution, is under pressure before hours after reporting second quarter EPS down 52% to 0.37 dollar, above estimates, from 0.74 dollar a year earlier. Net revenue declined 3% to 22.33 billion dollars.

Source: TradingView, Gain Capital

Morgan Stanley (MS), an investment firm, disclosed second quarter adjusted EPS of 2.04 dollars, beating estimates, from 1.23 dollar a year earlier, on revenue of 13.4 billion dollars from 10.2 billion dollars a year ago.

American Airlines (AAL), an airline company, announced that it has informed 25,000 U.S.-based employees of the possibility of a workforce reduction, saying it expects that these actions will take effect on or after October 1, 2020, and may continue through the end of 2020.

Dell Technologies (DELL), a multinational technology company, said it is exploring a potential spin-off of its 81% stake in software firm VMware (VMW), adding that any potential spin-off would not occur prior to September 2021.

Alcoa (AA), an aluminum giant, reported second quarter preliminary adjusted LPS of 0.02 dollar, at high end of forecast range, from an LPS of 0.01 a year ago on revenue of 2.15 billion dollars from 2.71 billion dollars in the prior-year period. Also, second quarter preliminary adjusted EBITDA was down to 185 million dollars from 455 million dollars last year.

Latest market news

Today 08:33 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM