U.S Futures slightly up - Watch BA, PFE, CAT, ISRG, SLB

The S&P 500 Futures are slightly up after they slipped for a third session yesterday. U.S. official data showed that Initial Jobless Claims unexpectedly jumped to 898,000 (825,000 expected), at the same time the government and Congress still failed to agree on a economic stimulus deal.

Later today, September retail sales (+0.8% on month expected) and August business inventories (+0.4% on month expected). The Federal Reserve will release September industrial production (+0.6% on month expected). The University of Michigan will publish its Consumer Sentiment Index for October (80.5 expected).

European indices are on the upside. Brexit talks made no progress as European Union negotiators called on the U.K. side to negotiate further. European leaders consider U.K. Prime Minister Boris Johnson threat to abandon Brexit talks today is a bluff. The European Commission has posted final readings of September CPI at -0.3% on year, as expected, and August trade balance at 21.9 billion euros surplus (vs 18 billion euros surplus expected).

Asian indices closed in the red except the Hong Kong HSI.

WTI Crude Oil futures are turning down. The U.S. Energy Information Administration Crude reported that crude stockpiles fell by 3.8 million barrels last week, more than a reduction of 2.8 million barrels expected. Besides, U.S. crude oil production dropped to 10.5 million barrels per day from 11.0 million barrels per day. Later today, Baker Hughes will report the total number of rig counts for the U.S. and Canada.

The dollar index fell 0.16pt to 93.698.

Gold and U.S dollar consolidate on uncertainty over U.S stimulus.

Gold rose 0.7 dollar (+0.04%) to 1909.41.

The dollar index fell 0.16pt to 93.698.

U.S. Equity Snapshot

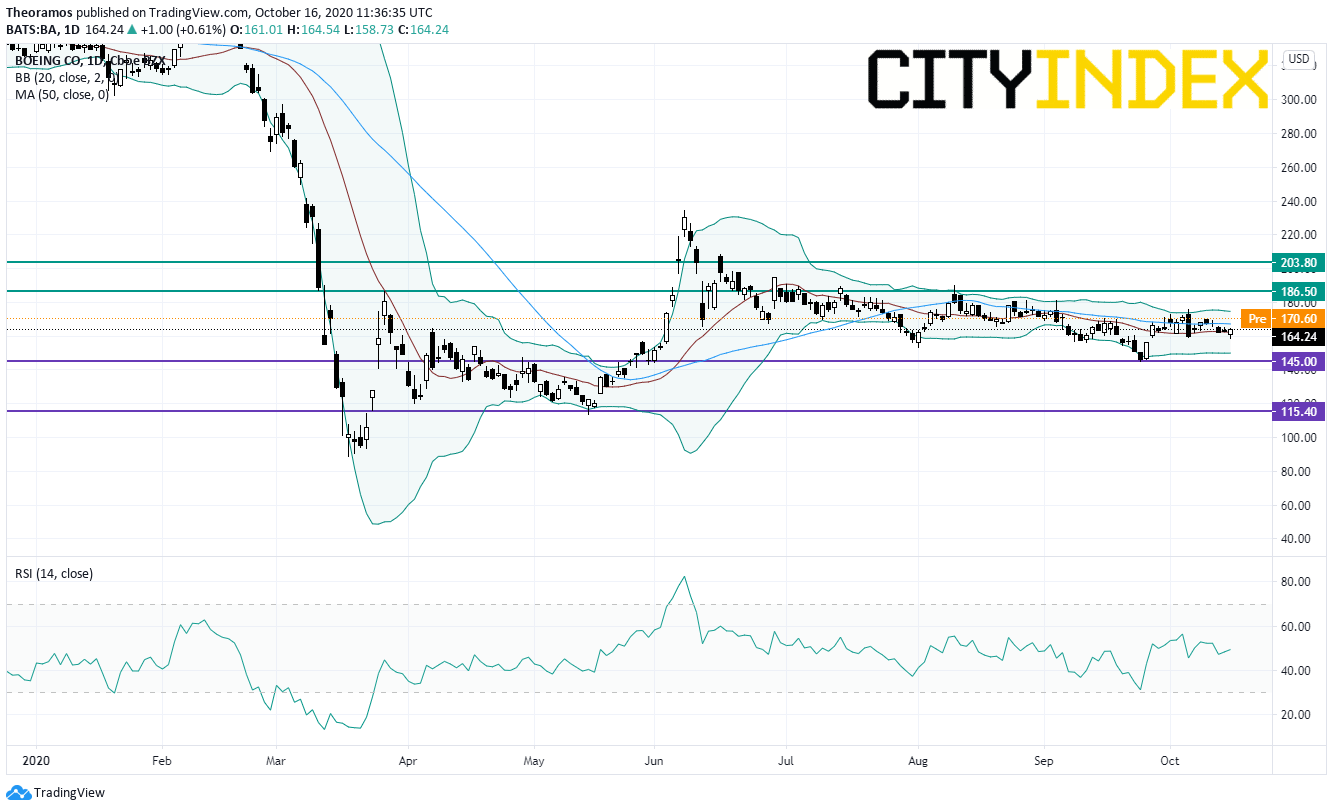

Boeing (BA), the aircraft maker, is expected to gain ground after Bloomberg reported that the European Union Aviation Safety Agency said that the 737 MAX is "safe" and could return to service before the end of 2020.

Caterpillar (CAT), the manufacturer of heavy equipment for multiple industries, was upgraded to "overweight" from "equal-weight" at Wells Fargo.

Intuitive Surgical (ISRG), a developer of robotic systems for the medical industry, slipped after hours after saying that "due to the continued uncertainty around the scope and duration of the pandemic and the timing of global recovery and economic normalization, we cannot, at this time, reliably estimate the future impact on our operations and financial results." Separately, the company posted third quarter earnings that beat estimates.

Schlumberger (SLB), the supplier of oil and gas products and services, is losing ground before hours after reporting third quarter sales that missed estimates.

Hewlett Packard Enterprise (HPE), an enterprise IT company, gained some ground in extended after unveiling it expects full year 2021 adjusted EPS of 1.56-1.76 dollar, exceeding estimates. The company confirmed its current year outlook.

Later today, September retail sales (+0.8% on month expected) and August business inventories (+0.4% on month expected). The Federal Reserve will release September industrial production (+0.6% on month expected). The University of Michigan will publish its Consumer Sentiment Index for October (80.5 expected).

European indices are on the upside. Brexit talks made no progress as European Union negotiators called on the U.K. side to negotiate further. European leaders consider U.K. Prime Minister Boris Johnson threat to abandon Brexit talks today is a bluff. The European Commission has posted final readings of September CPI at -0.3% on year, as expected, and August trade balance at 21.9 billion euros surplus (vs 18 billion euros surplus expected).

Asian indices closed in the red except the Hong Kong HSI.

WTI Crude Oil futures are turning down. The U.S. Energy Information Administration Crude reported that crude stockpiles fell by 3.8 million barrels last week, more than a reduction of 2.8 million barrels expected. Besides, U.S. crude oil production dropped to 10.5 million barrels per day from 11.0 million barrels per day. Later today, Baker Hughes will report the total number of rig counts for the U.S. and Canada.

The dollar index fell 0.16pt to 93.698.

Gold and U.S dollar consolidate on uncertainty over U.S stimulus.

Gold rose 0.7 dollar (+0.04%) to 1909.41.

The dollar index fell 0.16pt to 93.698.

U.S. Equity Snapshot

Boeing (BA), the aircraft maker, is expected to gain ground after Bloomberg reported that the European Union Aviation Safety Agency said that the 737 MAX is "safe" and could return to service before the end of 2020.

Source: TradingView, GAIN Capital

Pfizer (PFE), the pharma, said it could apply for US emergency use approval regarding its COVID-19 vaccine by late November.Caterpillar (CAT), the manufacturer of heavy equipment for multiple industries, was upgraded to "overweight" from "equal-weight" at Wells Fargo.

Intuitive Surgical (ISRG), a developer of robotic systems for the medical industry, slipped after hours after saying that "due to the continued uncertainty around the scope and duration of the pandemic and the timing of global recovery and economic normalization, we cannot, at this time, reliably estimate the future impact on our operations and financial results." Separately, the company posted third quarter earnings that beat estimates.

Schlumberger (SLB), the supplier of oil and gas products and services, is losing ground before hours after reporting third quarter sales that missed estimates.

Hewlett Packard Enterprise (HPE), an enterprise IT company, gained some ground in extended after unveiling it expects full year 2021 adjusted EPS of 1.56-1.76 dollar, exceeding estimates. The company confirmed its current year outlook.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM