EU indices under pressure | TA focus on Daimler

INDICES

Yesterday, European stocks end in the red. The Stoxx Europe 600 Index dropped 0.63%, Germany's DAX 30 fell 0.50%, France's CAC 40 slipped 0.61%, and the U.K.'s FTSE 100 shed 1.50%.

EUROPE ADVANCE/DECLINE

66% of STOXX 600 constituents traded lower or unchanged yesterday.

76% of the shares trade above their 20D MA vs 78% Wednesday (above the 20D moving average).

56% of the shares trade above their 200D MA vs 57% Wednesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 0.22pt to 22.69, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

health care, retail, technology

Europe worst 3 sectors

travel & leisure, energy, construction & materials

INTEREST RATE

The 10yr Bund yield rose 3bps to -0.45% (above its 20D MA). The 2yr-10yr yield spread fell 2bps to -23bps (below its 20D MA).

ECONOMIC DATA

FR 07:45: Jul Harmonised Inflation Rate MoM final, exp.: 0.1%

FR 07:45: Jul Inflation Rate YoY final, exp.: 0.2%

FR 07:45: Jul Inflation Rate MoM final, exp.: 0.1%

FR 07:45: Jul Harmonised Inflation Rate YoY final, exp.: 0.2%

EC 10:00: Q2 GDP Growth Rate YoY 2nd Est, exp.: -3.1%

EC 10:00: Q2 GDP Growth Rate QoQ 2nd Est, exp.: -3.6%

EC 10:00: Q2 Employment chg YoY Prel, exp.: 0.4%

EC 10:00: Q2 Employment chg QoQ Prel, exp.: -0.2%

EC 10:00: Jun Balance of Trade, exp.: E9.4B

MORNING TRADING

In Asian trading hours, EUR/USD eased to 1.1810 and GBP/USD fell to 1.3055. USD/JPY held gains at 106.94. AUD/USD slipped to 0.7139. Earlier today, official data showed that China's industrial production grew 4.8% on year in July (+5.1% expected) while retail sales dropped 1.1% (+0.1% expected).

Spot gold retreated to $1,951 an ounce.

#UK - IRELAND#

Domino's Pizza Group, a fast food pizza delivery chain, was downgraded to "sell" from "neutral" at Citigroup.

#GERMANY#

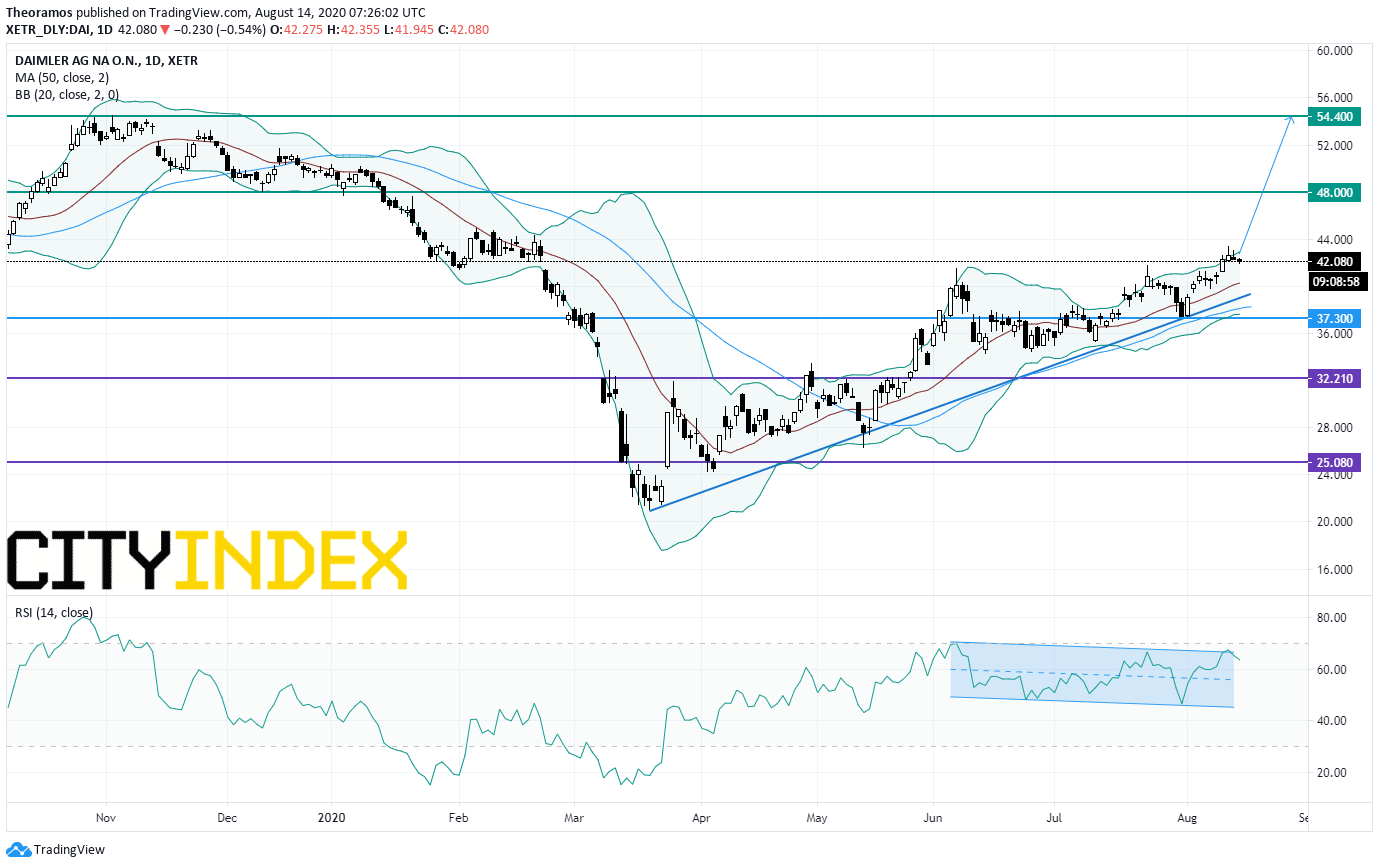

Daimler, an automobile group, said it expects costs of about 1.5 billion dollars for the settlements with the U.S. authorities, after reaching an agreement in principle regarding emission control systems of approximately 250,000 diesel passenger cars and vans in the country.

From a chartist point of view, the share has bypassed the horizontal resistance set at 41.5 (June & July highs). Furthermore, the 50-DMA and a rising trend line drawn since March are in support. In addition, the daily Relative Strength Index (RSI, 14) is escaping from a declining channel. Above 37.3E look for 48E and 54.4E in extension.

Source: GAIN Capital, TradingView

Hapag-Lloyd, a shipping and container transportation company, announced that 2Q net income jumped to 257 million euros from 46 million euros and EBITDA rose 49.8% on year to 699 million euros on revenue of 3.02 billion euros, down 5.0% on year. The company added: "Looking ahead, the results forecast remains unchanged. For the current financial year, Hapag-Lloyd expects an EBITDA of EUR 1.7 to 2.2 billion and an EBIT of EUR 0.5 to 1.0 billion."

Hella, an automotive part supplier, reported that it swung to a full-year net loss of 431 million euros from a net profit of 630 million euros and adjusted EBIT declined 59.3% on year to 233 million euros on revenue of 5.83 billion euros, down 16.6% (-14.3% currency and portfolio-adjusted). The company said: "As already announced at the end of July, HELLA anticipates for the current fiscal year 2020/2021 (1 June 2020 to 31 May 2021) consolidated sales adjusted for exchange rate and portfolio effects in a range between around E 5.6 billion and E 6.1 billion (previous year: E 5.7 billion)."

#FRANCE#

Arkema, a specialty chemicals firm, was downgraded to "hold" from "buy" at HSBC.

#SPAIN#

ACS, a civil and engineering construction group, is expected to report 1H results.

EX-DIVIDEND

Equinor (EQNR): $0.09, Novo Nordisk: DKK3.25

Yesterday, European stocks end in the red. The Stoxx Europe 600 Index dropped 0.63%, Germany's DAX 30 fell 0.50%, France's CAC 40 slipped 0.61%, and the U.K.'s FTSE 100 shed 1.50%.

EUROPE ADVANCE/DECLINE

66% of STOXX 600 constituents traded lower or unchanged yesterday.

76% of the shares trade above their 20D MA vs 78% Wednesday (above the 20D moving average).

56% of the shares trade above their 200D MA vs 57% Wednesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 0.22pt to 22.69, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

health care, retail, technology

Europe worst 3 sectors

travel & leisure, energy, construction & materials

INTEREST RATE

The 10yr Bund yield rose 3bps to -0.45% (above its 20D MA). The 2yr-10yr yield spread fell 2bps to -23bps (below its 20D MA).

ECONOMIC DATA

FR 07:45: Jul Harmonised Inflation Rate MoM final, exp.: 0.1%

FR 07:45: Jul Inflation Rate YoY final, exp.: 0.2%

FR 07:45: Jul Inflation Rate MoM final, exp.: 0.1%

FR 07:45: Jul Harmonised Inflation Rate YoY final, exp.: 0.2%

EC 10:00: Q2 GDP Growth Rate YoY 2nd Est, exp.: -3.1%

EC 10:00: Q2 GDP Growth Rate QoQ 2nd Est, exp.: -3.6%

EC 10:00: Q2 Employment chg YoY Prel, exp.: 0.4%

EC 10:00: Q2 Employment chg QoQ Prel, exp.: -0.2%

EC 10:00: Jun Balance of Trade, exp.: E9.4B

MORNING TRADING

In Asian trading hours, EUR/USD eased to 1.1810 and GBP/USD fell to 1.3055. USD/JPY held gains at 106.94. AUD/USD slipped to 0.7139. Earlier today, official data showed that China's industrial production grew 4.8% on year in July (+5.1% expected) while retail sales dropped 1.1% (+0.1% expected).

Spot gold retreated to $1,951 an ounce.

#UK - IRELAND#

Domino's Pizza Group, a fast food pizza delivery chain, was downgraded to "sell" from "neutral" at Citigroup.

#GERMANY#

Daimler, an automobile group, said it expects costs of about 1.5 billion dollars for the settlements with the U.S. authorities, after reaching an agreement in principle regarding emission control systems of approximately 250,000 diesel passenger cars and vans in the country.

From a chartist point of view, the share has bypassed the horizontal resistance set at 41.5 (June & July highs). Furthermore, the 50-DMA and a rising trend line drawn since March are in support. In addition, the daily Relative Strength Index (RSI, 14) is escaping from a declining channel. Above 37.3E look for 48E and 54.4E in extension.

Source: GAIN Capital, TradingView

Hapag-Lloyd, a shipping and container transportation company, announced that 2Q net income jumped to 257 million euros from 46 million euros and EBITDA rose 49.8% on year to 699 million euros on revenue of 3.02 billion euros, down 5.0% on year. The company added: "Looking ahead, the results forecast remains unchanged. For the current financial year, Hapag-Lloyd expects an EBITDA of EUR 1.7 to 2.2 billion and an EBIT of EUR 0.5 to 1.0 billion."

Hella, an automotive part supplier, reported that it swung to a full-year net loss of 431 million euros from a net profit of 630 million euros and adjusted EBIT declined 59.3% on year to 233 million euros on revenue of 5.83 billion euros, down 16.6% (-14.3% currency and portfolio-adjusted). The company said: "As already announced at the end of July, HELLA anticipates for the current fiscal year 2020/2021 (1 June 2020 to 31 May 2021) consolidated sales adjusted for exchange rate and portfolio effects in a range between around E 5.6 billion and E 6.1 billion (previous year: E 5.7 billion)."

#FRANCE#

Arkema, a specialty chemicals firm, was downgraded to "hold" from "buy" at HSBC.

#SPAIN#

ACS, a civil and engineering construction group, is expected to report 1H results.

EX-DIVIDEND

Equinor (EQNR): $0.09, Novo Nordisk: DKK3.25

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Commodities articles

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM

April 14, 2024 11:37 PM