U.S Futures up - Watch LYFT, BA, CVS

The S&P 500 Futures are on the upside after they closed mixed yesterday as the Dow Jones Industrial Average advanced a further 0.90% while the Nasdaq 100 shed another 1.74%.

No major economic data are expected today.

European indices remain on the upside.

Asian indices ended on a positive note except the Chinese CSI. The Reserve Bank of New Zealand kept its benchmark rate unchanged at 0.25% as expected. RBNZ said additional stimulus would be provided through a Funding for Lending Programme (FLP), commencing in December, and "monetary policy will need to remain stimulatory for a long time".

WTI Crude Oil remains strongly bullish. The American Petroleum Institute (API) reported that U.S. crude-oil inventories dropped 5.1M barrels in the week ending November 6. The U.S. Energy Information Administration (EIA) projected that 2021 WTI Crude Oil forecast price would be $44.24/bbl, down from $44.72 in the previous estimation. The global oil demand for 2021 lowered to 98.80M b/d from 99.09M b/d, while global supply is also down to 94.58M b/d from 98.83M b/d. Later today, EIA will release official crude oil inventories data for week ending November 6.

US indices closed mixed on Tuesday with the Dow Jones (+0.90%) closing up, while the Nasdaq (-1.37%) and S&P 500 (-0.14%) closed down. Automobiles & Components (+3.48%), Energy (+2.52%) and Food, Beverage & Tobacco (+2.4%) sectors were the best performers on the day, while Semiconductors & Semiconductor Equipment (-3.43%), Software & Services (-2.36%) and Retailing (-1.62%) sectors were the worst performers.

The dollar index rose 0.26pt to 93.011.

U.S. Equity Snapshot

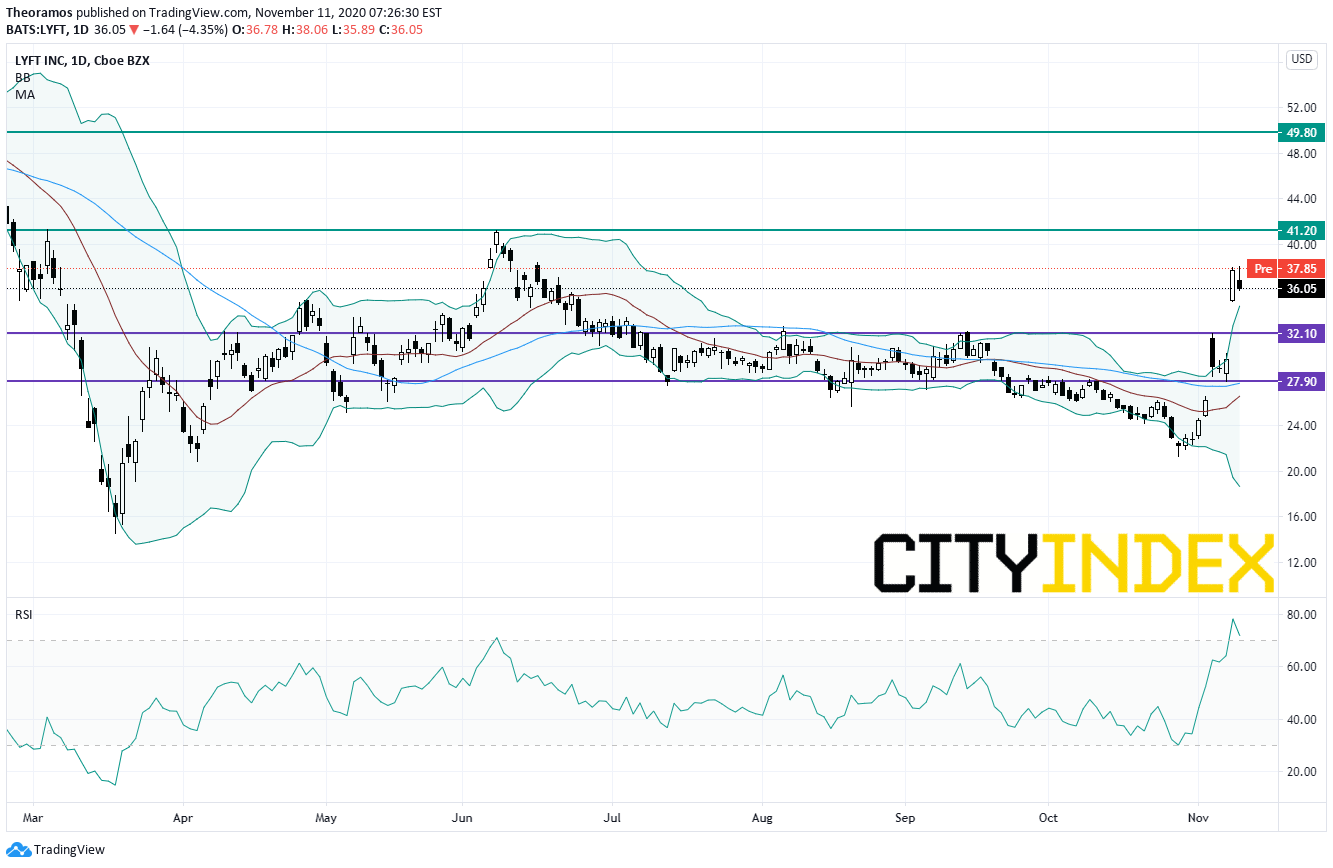

Lyft (LYFT), the ridesharing company, jumped after hours after reporting third quarter sales of 499.7 million dollars, above forecasts, down from 955.6 million dollars last year. LPS was 1.46 dollar, worse than expected, vs a LPS of 0.41 dollar a year ago. The company expects Ebitda to be positive by the fourth quarter of 2021.

Source: TradingView, GAIN Capital

Boeing (BA) won a 9.8 billion dollars contract from the Pentagon regarding F-15 support for Saudi Arabia.

CVS Health's (CVS), the pharmacy and healthcare company, price target was raised to 76 dollars from 72 dollars at Piper Sandler.

No major economic data are expected today.

European indices remain on the upside.

Asian indices ended on a positive note except the Chinese CSI. The Reserve Bank of New Zealand kept its benchmark rate unchanged at 0.25% as expected. RBNZ said additional stimulus would be provided through a Funding for Lending Programme (FLP), commencing in December, and "monetary policy will need to remain stimulatory for a long time".

WTI Crude Oil remains strongly bullish. The American Petroleum Institute (API) reported that U.S. crude-oil inventories dropped 5.1M barrels in the week ending November 6. The U.S. Energy Information Administration (EIA) projected that 2021 WTI Crude Oil forecast price would be $44.24/bbl, down from $44.72 in the previous estimation. The global oil demand for 2021 lowered to 98.80M b/d from 99.09M b/d, while global supply is also down to 94.58M b/d from 98.83M b/d. Later today, EIA will release official crude oil inventories data for week ending November 6.

US indices closed mixed on Tuesday with the Dow Jones (+0.90%) closing up, while the Nasdaq (-1.37%) and S&P 500 (-0.14%) closed down. Automobiles & Components (+3.48%), Energy (+2.52%) and Food, Beverage & Tobacco (+2.4%) sectors were the best performers on the day, while Semiconductors & Semiconductor Equipment (-3.43%), Software & Services (-2.36%) and Retailing (-1.62%) sectors were the worst performers.

Approximately 82% of stocks in the S&P 500 Index were trading above their 200-day moving average and 78% were trading above their 20-day moving average. The VIX Index dropped 1.23pt (-4.78%) to 24.52 and WTI Crude Oil gained $1.09 (+2.71%) to $41.38 at the close.

On the US economic data front, the National Federation of Independent Business's Small Business Optimism Index remained unchanged at 104.0 on month in October (104.1 expected), in line with September. Finally, U.S. Job Openings rose to 6.436 million on month in September (6.500 million expected), compared to a revised 6.352 million in August.Gold loses ground as the U.S dollar remains firm on return for risk appetite.

Gold fell 1.48 dollar (-0.08%) to 1875.85 dollars.The dollar index rose 0.26pt to 93.011.

U.S. Equity Snapshot

Lyft (LYFT), the ridesharing company, jumped after hours after reporting third quarter sales of 499.7 million dollars, above forecasts, down from 955.6 million dollars last year. LPS was 1.46 dollar, worse than expected, vs a LPS of 0.41 dollar a year ago. The company expects Ebitda to be positive by the fourth quarter of 2021.

Source: TradingView, GAIN Capital

Boeing (BA) won a 9.8 billion dollars contract from the Pentagon regarding F-15 support for Saudi Arabia.

CVS Health's (CVS), the pharmacy and healthcare company, price target was raised to 76 dollars from 72 dollars at Piper Sandler.

Latest market news

Today 08:18 AM

Yesterday 10:40 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM