EU indices significantly up | TA focus on Zalando

INDICES

Yesterday, European stocks were slightly up. The Stoxx Europe 600 Index climbed 0.30%, Germany's DAX 30 edged up 0.10%, France's CAC 40 gained 0.41% and the U.K.'s FTSE 100 was up 0.31%.

EUROPE ADVANCE/DECLINE

57% of STOXX 600 constituents traded higher yesterday.

54% of the shares trade above their 20D MA vs 50% Friday (below the 20D moving average).

50% of the shares trade above their 200D MA vs 49% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 0.09pt to 24.11, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Construction, Industrial

3mths relative low: Healthcare

Europe Best 3 sectors

banks, energy, insurance

Europe worst 3 sectors

technology, health care, retail

INTEREST RATE

The 10yr Bund yield rose 2bps to -0.51% (below its 20D MA). The 2yr-10yr yield spread fell 0bp to -18bps (above its 20D MA).

ECONOMIC DATA

UK 07:00: May Employment chg, exp.: -126K

UK 07:00: Jun Average Earnings excl. Bonus, exp.: 0.7%

UK 07:00: Jun Average Earnings incl. Bonus, exp.: -0.3%

UK 07:00: Jun Unemployment Rate, exp.: 3.9%

UK 07:00: Jul Claimant Count chg, exp.: -28.1K

EC 10:00: Aug ZEW Economic Sentiment Idx, exp.: 59.6

GE 10:00: Aug ZEW Current Conditions, exp.: -80.9

GE 10:00: Aug ZEW Economic Sentiment Idx, exp.: 59.3

UK 10:45: 5-Year Treasury Gilt auction, exp.: -0.03%

MORNING TRADING

In Asian trading hours, EUR/USD was little changed at 1.1745 while GBP/USD advanced further to 1.3083. USD/JPY climbed above 106.00 level.

Spot gold dropped to $2,016 an ounce.

#UK - IRELAND#

Gamesys Group, an online software development and gaming business, released 1H results: "Reported gaming revenue grew 101% year-on-year, (...) Adjusted EBITDA increased 75% year-on-year; (...) Adjusted net income1,2,4 increased 68% year-on-year. (...) The Board is pleased to declare an inaugural interim dividend of 12p per share to be paid in October."

Prudential, an insurance group, is expected to report 1H results.

HSBC, a global banking group, was upgraded to "equalweight" from "underweight" at Morgan Stanley.

3i Group, a private equity and venture capital company, was upgraded to "overweight" from "equalweight" at Morgan Stanley.

#GERMANY#

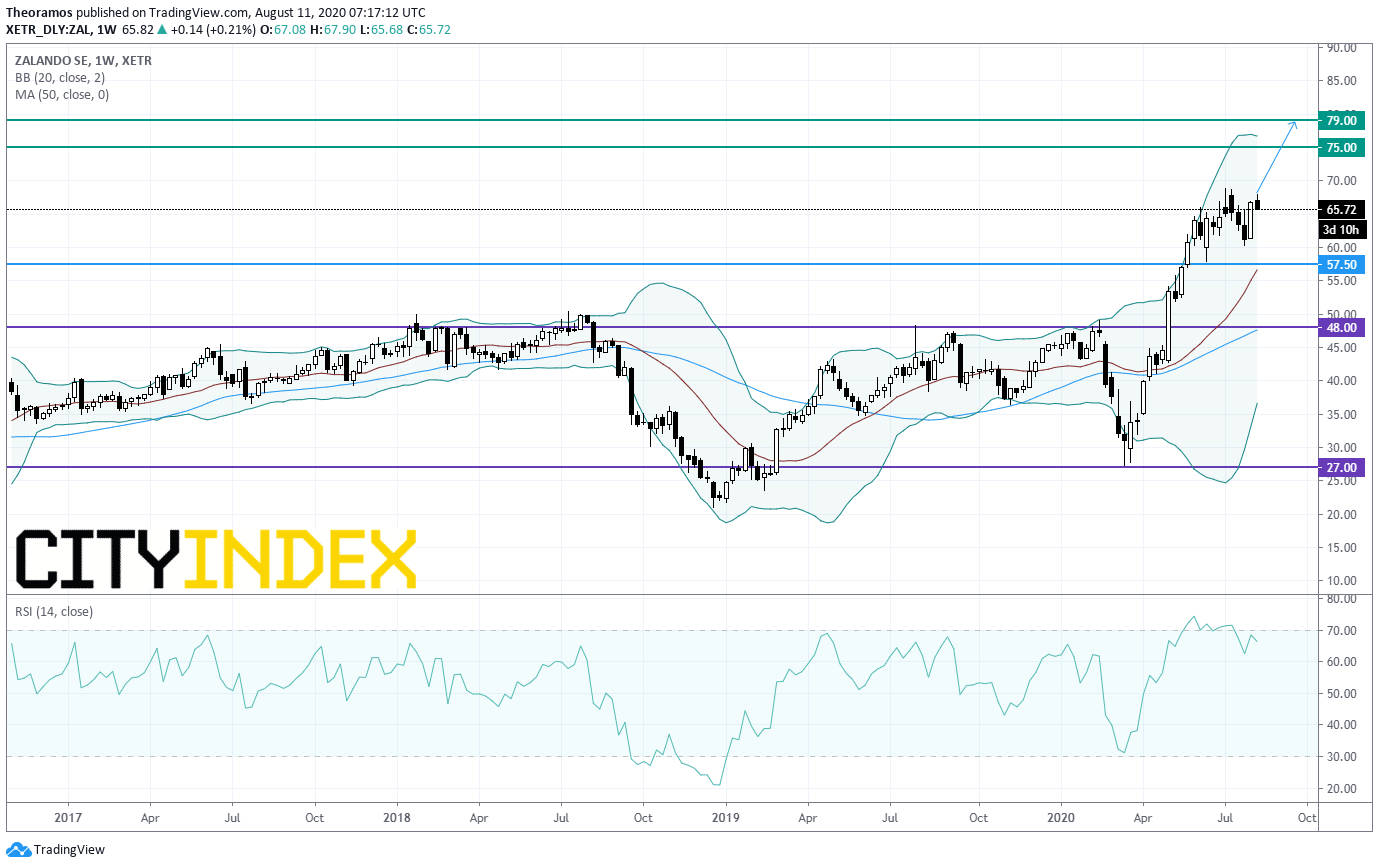

Zalando, an e-commerce company, announced that 2Q net income jumped to 123 million euros from 46 million euros in the prior-year period and adjusted EBIT surged to 212 million euros from 102 million euros. Also, revenue was up 27.4% on year to 2.03 billion euros. The company confirmed its full-year revenue growth guidance of 15-20% and adjusted EBIT forecast of between 250-300 million euros.

From a weekly point of view, the share is consolidating but remains strongly bullish above the key resistance in place since 2018 at 48E. Above 57.5E, look for 75E and 79E in extension.

Source: GAIN Capital, TradingView

Uniper, an energy company, posted 1H adjusted net income jumped to 527 million euros from 189 million euros in the prior-year period and adjusted EBIT climbed to 691 million euros from 308 million euros. The company said: "Uniper now anticipates adjusted EBIT of E800 million to E1 billion and adjusted net income of E600 million to E800 million."

#FRANCE#

Thales, an aerospace and defence company, was upgraded to "overweight" from "neutral" at JPMorgan.

#DENMARK#

Vestas Wind Systems, a wind turbines manufacturer, reported that it swung to a 2Q net loss of 5 million euros from a net profit of 90 million euros in the prior-year period and operating EBIT dropped to 34 million euros from 128 million euros on revenue of 3.54 billion euros, up 66.9%. The company said "the outlook for full-year revenue is unchanged at EUR 14-15bn".

Yesterday, European stocks were slightly up. The Stoxx Europe 600 Index climbed 0.30%, Germany's DAX 30 edged up 0.10%, France's CAC 40 gained 0.41% and the U.K.'s FTSE 100 was up 0.31%.

EUROPE ADVANCE/DECLINE

57% of STOXX 600 constituents traded higher yesterday.

54% of the shares trade above their 20D MA vs 50% Friday (below the 20D moving average).

50% of the shares trade above their 200D MA vs 49% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 0.09pt to 24.11, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Construction, Industrial

3mths relative low: Healthcare

Europe Best 3 sectors

banks, energy, insurance

Europe worst 3 sectors

technology, health care, retail

INTEREST RATE

The 10yr Bund yield rose 2bps to -0.51% (below its 20D MA). The 2yr-10yr yield spread fell 0bp to -18bps (above its 20D MA).

ECONOMIC DATA

UK 07:00: May Employment chg, exp.: -126K

UK 07:00: Jun Average Earnings excl. Bonus, exp.: 0.7%

UK 07:00: Jun Average Earnings incl. Bonus, exp.: -0.3%

UK 07:00: Jun Unemployment Rate, exp.: 3.9%

UK 07:00: Jul Claimant Count chg, exp.: -28.1K

EC 10:00: Aug ZEW Economic Sentiment Idx, exp.: 59.6

GE 10:00: Aug ZEW Current Conditions, exp.: -80.9

GE 10:00: Aug ZEW Economic Sentiment Idx, exp.: 59.3

UK 10:45: 5-Year Treasury Gilt auction, exp.: -0.03%

MORNING TRADING

In Asian trading hours, EUR/USD was little changed at 1.1745 while GBP/USD advanced further to 1.3083. USD/JPY climbed above 106.00 level.

Spot gold dropped to $2,016 an ounce.

#UK - IRELAND#

Gamesys Group, an online software development and gaming business, released 1H results: "Reported gaming revenue grew 101% year-on-year, (...) Adjusted EBITDA increased 75% year-on-year; (...) Adjusted net income1,2,4 increased 68% year-on-year. (...) The Board is pleased to declare an inaugural interim dividend of 12p per share to be paid in October."

Prudential, an insurance group, is expected to report 1H results.

HSBC, a global banking group, was upgraded to "equalweight" from "underweight" at Morgan Stanley.

3i Group, a private equity and venture capital company, was upgraded to "overweight" from "equalweight" at Morgan Stanley.

#GERMANY#

Zalando, an e-commerce company, announced that 2Q net income jumped to 123 million euros from 46 million euros in the prior-year period and adjusted EBIT surged to 212 million euros from 102 million euros. Also, revenue was up 27.4% on year to 2.03 billion euros. The company confirmed its full-year revenue growth guidance of 15-20% and adjusted EBIT forecast of between 250-300 million euros.

From a weekly point of view, the share is consolidating but remains strongly bullish above the key resistance in place since 2018 at 48E. Above 57.5E, look for 75E and 79E in extension.

Source: GAIN Capital, TradingView

Uniper, an energy company, posted 1H adjusted net income jumped to 527 million euros from 189 million euros in the prior-year period and adjusted EBIT climbed to 691 million euros from 308 million euros. The company said: "Uniper now anticipates adjusted EBIT of E800 million to E1 billion and adjusted net income of E600 million to E800 million."

#FRANCE#

Thales, an aerospace and defence company, was upgraded to "overweight" from "neutral" at JPMorgan.

#DENMARK#

Vestas Wind Systems, a wind turbines manufacturer, reported that it swung to a 2Q net loss of 5 million euros from a net profit of 90 million euros in the prior-year period and operating EBIT dropped to 34 million euros from 128 million euros on revenue of 3.54 billion euros, up 66.9%. The company said "the outlook for full-year revenue is unchanged at EUR 14-15bn".

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM