U.S Futures sliding - Watch CVS, SQ, UBER, ROKU, EA

The S&P 500 Futures are drawing a consolidation after four straight days of rally as investors still face uncertainty of the presidential election result.

Later today, the U.S. Labor Department will release the nonfarm payrolls report for October (+0.59 million jobs, jobless rate at 7.6% expected). The Commerce Department will report September wholesale inventories (-0.1% on month expected).

European indices are losing some ground. On the economic data front, German September industrial production only rose 1.6% on month while +2.5% was expected August figures have been revised lower from +0.5% to +0.2%.

Asian indices closed higher. In japan, official data showed that household spending dropped 10.2% on year in September (-10.5% expected).

WTI Crude Oil is still consolidating during Asian session. RBC expected that Iran would return to oil exported by 2H next year if former President Job Biden wins the President election. Besides, Standard Chartered Bank projected that global oil demand would fall by 8.73M b/d on year in 4Q. Later today, Baker Hughes will report the total number of rig counts for the U.S. and Canada.

Gold is on set for a weekly gain while the U.S dollar still consolidates on risks of divided U.S congress and hopes of further Fed stimulus.

Gold rose 6.14 dollars (+0.32%) to 1955.81.

The dollar index fell 0.2pt to 92.322.

U.S. Equity Snapshot

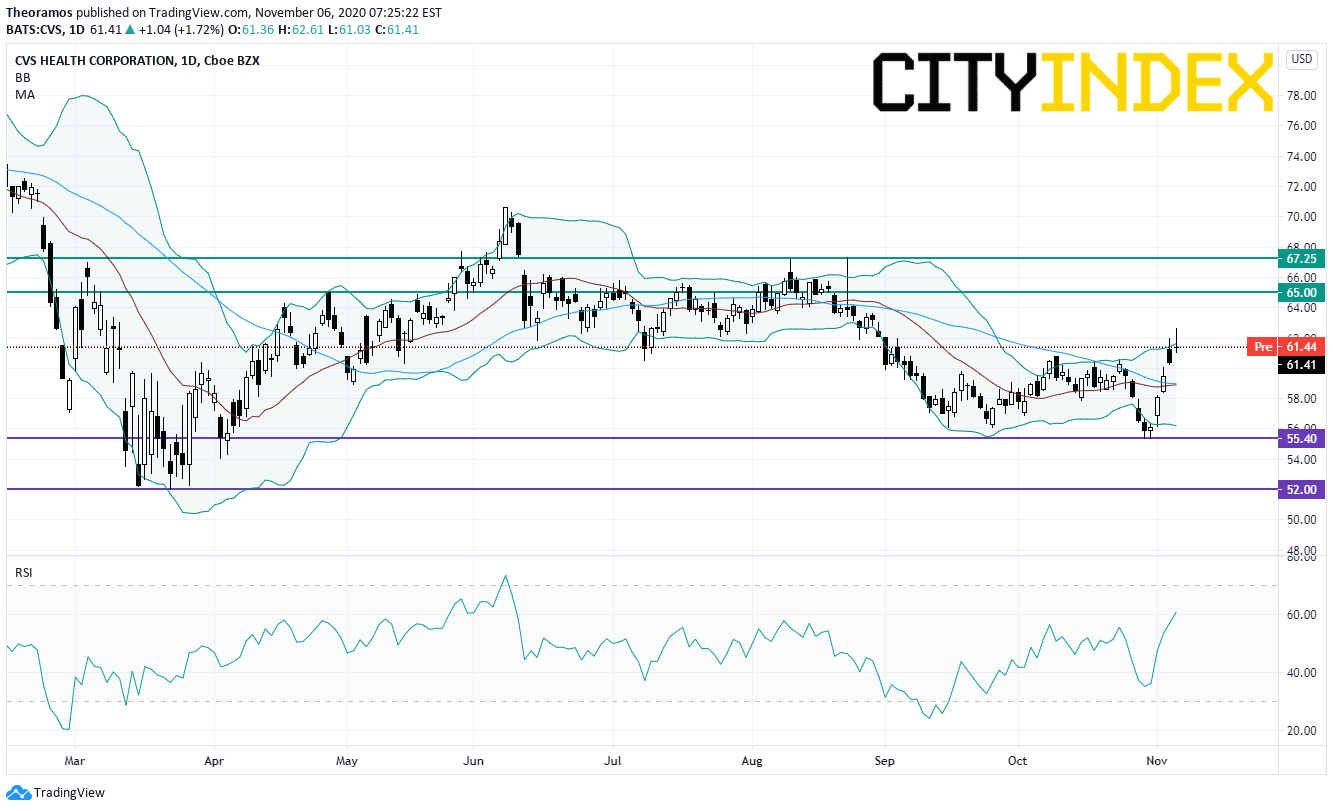

CVS Health (CVS), the pharmacy and healthcare company, pops before premarket after reporting third quarter adjusted EPS of 1.66 dollar, above estimates, vs 1.84 dollar a year earlier, on comparable sales up 5.7%, beating forecasts. The company expects full year adjusted EPS of 7.35-7.45 dollars, exceeding consensus, vs a previous forecast of 7.14-7.27 dollars. Separately, the company "appointed Karen S. Lynch, currently Executive Vice President, CVS Health and President, Aetna, as the company's next President and CEO, effective February 1, 2021."

Source: TradingView, GAIN Capital

Square (SQ), the mobile and electronic payment specialist, jumped after hours after posting quarterly adjusted EPS that significantly beat estimates.

Uber Technologies (UBER), the ride-sharing company, lost ground post market as third quarter sales missed estimates.

Roku (ROKU), the video streaming platform, gained ground in extended trading after reporting third quarter earnings that beat estimates.

Electronic Arts (EA), a global developer and publisher of video games, posted second quarter adjusted EPS of 0.05 dollar, just ahead of the consensus, down from 0.97 dollar a year ago on adjusted revenue of 910.0 million dollars, below forecasts, down from 1.3 billion dollars a year earlier.

T-Mobile US (TMUS), a wireless network operator, released third quarter EPS of 1.00 dollar, beating forecasts, down from 1.15 dollar a year ago on revenue of 19.3 billion dollars, better than expected, up from 11.1 billion dollars a year earlier.

Peloton Interactive (PTON), the interactive fitness platform, dropped post market as the company warned of delivering delays and increasing costs.

Zillow (ZG), the online real estate database company, jumped after hours as third quarter earnings topped estimates.

Booking Holdings (BKNG), one of the largest online travel companies, reported third quarter adjusted EPS of 12.27 dollars, missing estimates, down from 45.36 dollars a year ago on revenue of 2.6 billion dollars, above forecasts, down from 5.0 billion dollars a year earlier.

AIG (AIG), a global insurance and financial services firm, announced third quarter adjusted EPS of 0.81 dollar, beating forecasts, up from 0.56 dollar a year ago.

Monster Beverage (MNST), a developer and marketer of energy drinks, disclosed third quarter EPS of 0.65 dollar, just above estimates, up from 0.55 dollar a year ago on sales of 1.3 billion dollars, also just beating the consensus, up from 1.1 billion dollars a year earlier.

Later today, the U.S. Labor Department will release the nonfarm payrolls report for October (+0.59 million jobs, jobless rate at 7.6% expected). The Commerce Department will report September wholesale inventories (-0.1% on month expected).

European indices are losing some ground. On the economic data front, German September industrial production only rose 1.6% on month while +2.5% was expected August figures have been revised lower from +0.5% to +0.2%.

Asian indices closed higher. In japan, official data showed that household spending dropped 10.2% on year in September (-10.5% expected).

WTI Crude Oil is still consolidating during Asian session. RBC expected that Iran would return to oil exported by 2H next year if former President Job Biden wins the President election. Besides, Standard Chartered Bank projected that global oil demand would fall by 8.73M b/d on year in 4Q. Later today, Baker Hughes will report the total number of rig counts for the U.S. and Canada.

U.S indices closed up on Thursday, lifted by Automobiles & Components (+5.05%), Materials (+4.05%) and Semiconductors & Semiconductor Equipment (+4.04%) sectors.

Approximately 72% of stocks in the S&P 500 Index were trading above their 200-day moving average and 49% were trading above their 20-day moving average. The VIX Index fell 1.77pt (-5.99%) to 27.8 and WTI Crude Oil declined $0.64 (-1.63%) to $38.51 at the close.

On the U.S economic data front, Initial Jobless Claims dropped to 751K for the week ending October 31st (735K expected), from a revised 758K in the week before. Continuing Claims fell to 7,285K for the week ending October 24th (7,200K expected), from a revised 7,823K in the prior week. Finally, the Federal Open Market Committee (FOMC) kept the Federal Funds Target Rate between 0.00% and 0.25%, as expected.

Gold is on set for a weekly gain while the U.S dollar still consolidates on risks of divided U.S congress and hopes of further Fed stimulus.

Gold rose 6.14 dollars (+0.32%) to 1955.81.

The dollar index fell 0.2pt to 92.322.

U.S. Equity Snapshot

CVS Health (CVS), the pharmacy and healthcare company, pops before premarket after reporting third quarter adjusted EPS of 1.66 dollar, above estimates, vs 1.84 dollar a year earlier, on comparable sales up 5.7%, beating forecasts. The company expects full year adjusted EPS of 7.35-7.45 dollars, exceeding consensus, vs a previous forecast of 7.14-7.27 dollars. Separately, the company "appointed Karen S. Lynch, currently Executive Vice President, CVS Health and President, Aetna, as the company's next President and CEO, effective February 1, 2021."

Source: TradingView, GAIN Capital

Square (SQ), the mobile and electronic payment specialist, jumped after hours after posting quarterly adjusted EPS that significantly beat estimates.

Uber Technologies (UBER), the ride-sharing company, lost ground post market as third quarter sales missed estimates.

Roku (ROKU), the video streaming platform, gained ground in extended trading after reporting third quarter earnings that beat estimates.

Electronic Arts (EA), a global developer and publisher of video games, posted second quarter adjusted EPS of 0.05 dollar, just ahead of the consensus, down from 0.97 dollar a year ago on adjusted revenue of 910.0 million dollars, below forecasts, down from 1.3 billion dollars a year earlier.

T-Mobile US (TMUS), a wireless network operator, released third quarter EPS of 1.00 dollar, beating forecasts, down from 1.15 dollar a year ago on revenue of 19.3 billion dollars, better than expected, up from 11.1 billion dollars a year earlier.

Peloton Interactive (PTON), the interactive fitness platform, dropped post market as the company warned of delivering delays and increasing costs.

Zillow (ZG), the online real estate database company, jumped after hours as third quarter earnings topped estimates.

Booking Holdings (BKNG), one of the largest online travel companies, reported third quarter adjusted EPS of 12.27 dollars, missing estimates, down from 45.36 dollars a year ago on revenue of 2.6 billion dollars, above forecasts, down from 5.0 billion dollars a year earlier.

AIG (AIG), a global insurance and financial services firm, announced third quarter adjusted EPS of 0.81 dollar, beating forecasts, up from 0.56 dollar a year ago.

Monster Beverage (MNST), a developer and marketer of energy drinks, disclosed third quarter EPS of 0.65 dollar, just above estimates, up from 0.55 dollar a year ago on sales of 1.3 billion dollars, also just beating the consensus, up from 1.1 billion dollars a year earlier.

Latest market news

Today 08:18 AM

Yesterday 10:40 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM