EU indices still positive | TA focus on Aviva

INDICES

Yesterday, European stocks were broadly higher. The Stoxx Europe 600 Index rose 0.49%, Germany's DAX 30 climbed 0.47%, France's CAC 40 gained 0.90%, and the U.K.'s FTSE 100 jumped 1.14%.

EUROPE ADVANCE/DECLINE

75% of STOXX 600 constituents traded higher yesterday.

54% of the shares trade above their 20D MA vs 41% Tuesday (below the 20D moving average).

50% of the shares trade above their 200D MA vs 47% Tuesday (below the 20D moving average).

The Euro Stoxx 50 Volatility index eased 1.14pt to 23.94, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Industrial, Basic Resource

3mths relative low: Telecom.

Europe Best 3 sectors

basic resources, travel & leisure, energy

Europe worst 3 sectors

food & beverage, health care, telecommunications

INTEREST RATE

The 10yr Bund yield fell 3bps to -0.55% (below its 20D MA). The 2yr-10yr yield spread fell 4bps to -19bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Jun Factory Orders MoM, exp.: 10.4%

UK 07:00: BoE Inflation Report

UK 07:00: BoE Interest Rate Decision, exp.: 0.1%

UK 07:00: BoE Quantitative Easing, exp.: £745B

UK 07:00: MPC Meeting Minutes

UK 07:00: BoE MPC Vote Hike, exp.: 0/9

UK 07:00: BoE MPC Vote Unchanged, exp.: 44083

UK 07:00: BoE MPC Vote Cut, exp.: 0/9

EC 08:30: Jul Construction PMI, exp.: 48.3

FR 08:30: Jul Construction PMI, exp.: 53.8

GE 08:30: Jul Construction PMI, exp.: 41.3

UK 09:30: Jul Construction PMI, exp.: 55.3

FR 10:00: 3-Year BTAN auction, exp.: -0.58%

FR 10:00: 5-Year BTAN auction, exp.: -0.45%

FR 10:00: 10-Year OAT auction, exp.: -0.09%

GE 17:00: Bundesbank Beermann speech

MORNING TRADING

In Asian trading hours, the U.S. dollar stabilized. EUR/USD failed to climbed back to 1.1900 on the upside. GBP/USD stayed at levels around 1.3130. USD/JPY showed no signs of a sustainable rebound trading at 105.50.

Spot gold ran up to $2,031 an ounce before entering a consolidation phase.

#UK - IRELAND#

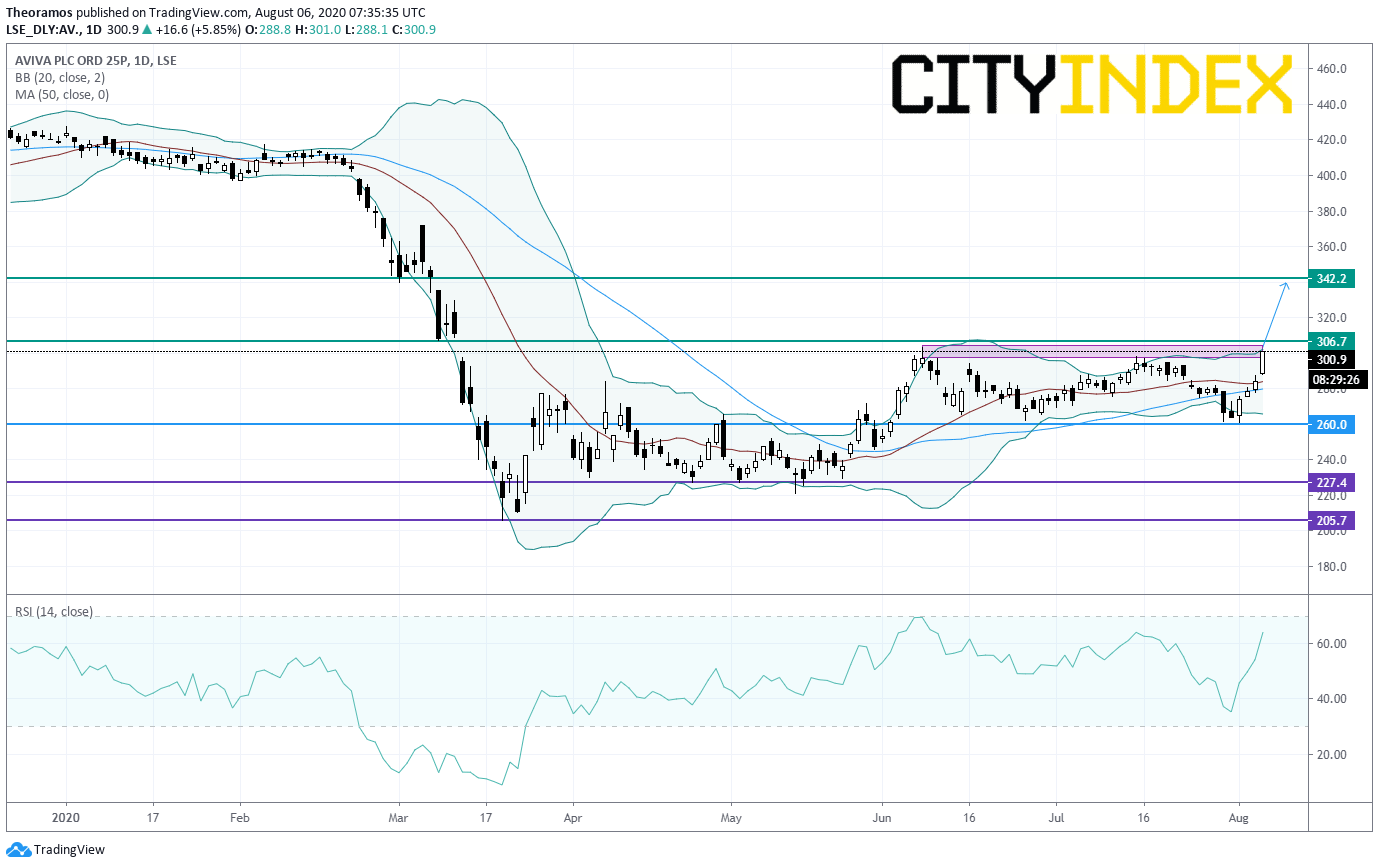

Aviva, a global insurance firm, posted 1H results: "Operating profit was 1,225 million pounds (HY19: 1,386 million pounds) while basic earnings per share fell to 20.0 pence (HY19 28.2 pence). Excluding COVID-19 impacts on general insurance claims (165 million pounds), operating profit was flat year on year, with strong results in UK annuities and the continued recovery in our Canadian results offset by higher weather claims across our general insurance businesses and additional expenditure related to community support initiatives. (...) The Board has declared a second interim dividend in respect of the 2019 financial year of 6 pence per share. (...) we have decided to take the opportunity to review our longer term dividend policy, (...) We will update shareholders on all dividend matters, including the 2019 final dividend in the fourth quarter."

From a daily point of view, the share is trying to escape from a consolidation area in place since June. Furthermore, Bollinger Bands are widening. Above 260p targets are set at the resistance at the level of March 2020 at 306.7p and 342.2p in extension.

Source: GAIN Capital, TradingView

Yesterday, European stocks were broadly higher. The Stoxx Europe 600 Index rose 0.49%, Germany's DAX 30 climbed 0.47%, France's CAC 40 gained 0.90%, and the U.K.'s FTSE 100 jumped 1.14%.

EUROPE ADVANCE/DECLINE

75% of STOXX 600 constituents traded higher yesterday.

54% of the shares trade above their 20D MA vs 41% Tuesday (below the 20D moving average).

50% of the shares trade above their 200D MA vs 47% Tuesday (below the 20D moving average).

The Euro Stoxx 50 Volatility index eased 1.14pt to 23.94, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Industrial, Basic Resource

3mths relative low: Telecom.

Europe Best 3 sectors

basic resources, travel & leisure, energy

Europe worst 3 sectors

food & beverage, health care, telecommunications

INTEREST RATE

The 10yr Bund yield fell 3bps to -0.55% (below its 20D MA). The 2yr-10yr yield spread fell 4bps to -19bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Jun Factory Orders MoM, exp.: 10.4%

UK 07:00: BoE Inflation Report

UK 07:00: BoE Interest Rate Decision, exp.: 0.1%

UK 07:00: BoE Quantitative Easing, exp.: £745B

UK 07:00: MPC Meeting Minutes

UK 07:00: BoE MPC Vote Hike, exp.: 0/9

UK 07:00: BoE MPC Vote Unchanged, exp.: 44083

UK 07:00: BoE MPC Vote Cut, exp.: 0/9

EC 08:30: Jul Construction PMI, exp.: 48.3

FR 08:30: Jul Construction PMI, exp.: 53.8

GE 08:30: Jul Construction PMI, exp.: 41.3

UK 09:30: Jul Construction PMI, exp.: 55.3

FR 10:00: 3-Year BTAN auction, exp.: -0.58%

FR 10:00: 5-Year BTAN auction, exp.: -0.45%

FR 10:00: 10-Year OAT auction, exp.: -0.09%

GE 17:00: Bundesbank Beermann speech

MORNING TRADING

In Asian trading hours, the U.S. dollar stabilized. EUR/USD failed to climbed back to 1.1900 on the upside. GBP/USD stayed at levels around 1.3130. USD/JPY showed no signs of a sustainable rebound trading at 105.50.

Spot gold ran up to $2,031 an ounce before entering a consolidation phase.

#UK - IRELAND#

Aviva, a global insurance firm, posted 1H results: "Operating profit was 1,225 million pounds (HY19: 1,386 million pounds) while basic earnings per share fell to 20.0 pence (HY19 28.2 pence). Excluding COVID-19 impacts on general insurance claims (165 million pounds), operating profit was flat year on year, with strong results in UK annuities and the continued recovery in our Canadian results offset by higher weather claims across our general insurance businesses and additional expenditure related to community support initiatives. (...) The Board has declared a second interim dividend in respect of the 2019 financial year of 6 pence per share. (...) we have decided to take the opportunity to review our longer term dividend policy, (...) We will update shareholders on all dividend matters, including the 2019 final dividend in the fourth quarter."

From a daily point of view, the share is trying to escape from a consolidation area in place since June. Furthermore, Bollinger Bands are widening. Above 260p targets are set at the resistance at the level of March 2020 at 306.7p and 342.2p in extension.

Source: GAIN Capital, TradingView

#GERMANY#

Siemens, a German industrial conglomerate, reported that 3Q net income shrank to 539 million euros from 1.03 billion euros in the prior-year period, saying: "Discontinued operations turned sharply negative due mainly to losses at Siemens Gamesa Renewable Energy driven by impacts related to COVID-19." 3Q Adjusted EBITA Industrial Business grew 8% on year to 1.79 billion euros, as total revenue was down 5% to 13.49 billion euros. It added: "Siemens expects the economic consequences of the COVID-19 pandemic to continue to strongly impact its fiscal fourth quarter financial results. (...) The company continues to expect a moderate decline in comparable revenue in fiscal 2020."

Merck KGaA, a global pharmaceutical firm, reported that 2Q after-tax profit dropped 38.6% on year to 289 million euros (adjusted earnings per share -15.6% to 1.30 euros) on sales of 4.12 billion euros, up 3.7%. 2Q Adjusted EBITDA declined 5.7% to 1.07 billion euros. The Company said it now expects full-year Adjusted EBITDA to be between 4.45 billion euros (4.35 billion euros previously) and 4.85 billion euros.

Henkel, a chemical company, said 1H Adjusted EBIT dropped 27.5% on year to 1.64 billion euros on sales of 9.49 billion euros, down 6.0% (-5.2% organic decline). The Company pointed out: "Adhesive Technologies was impacted primarily by significantly declining demand from key customer industries. Beauty Care performance was affected mostly by the significantly negative Hair Salon business, driven by the salon closures enforced in numerous countries. Laundry & Home Care showed a very strong development."

Adidas, a major maker of sports footwear and apparel, announced that it swung to a 2Q net loss of 295 million euros from a net income of 531 million euros in the prior-year period. 2Q net sales declined 35% to 3.58 billion euros. The Company pointed out: "adidas recorded a material revenue decline in its physical distribution channels during the second quarter of 2020 as the global coronavirus pandemic caused a very large number of store closures (...) Sales through the company’s own e-commerce channel increased 93% during the quarter."

Deutsche Lufthansa, a major German airline, reported that it swung to a 2Q net loss of 1.50 billion euros from a net income of 226 million euros in the prior-year period. 2Q Adjusted EBIT ran into a loss of 1.7 billion euros from a profit of 754 million euros on revenue of 1.9 billion euros, down 80% on year. The Company said: "Despite the capacity expansion, the Lufthansa Group also expects a clearly negative Adjusted EBIT in the second half of 2020 and thus a further significant decline in Adjusted EBIT for the full year."

Beiersdorf, which produces skin and hair care products, reported that 1H net income dropped to 285 million euros from 410 million euros in the prior-year period.

Rheinmetall, a German defense firm, said 1H operating earnings sank to 70 million euros from 163 million euros in the prior-year period on sales of 2.60 billion euros, down 7.7%.

#BENELUX#

ING Groep, a Dutch financial institution, reported that 2Q net income tumbled to 299 million euros from 1.44 billion euros in the prior-year period, citing an impairment charge of 300 million euros related to impacts caused by the coronavirus pandemic.

KBC, a Brussels-based bank, posted 2Q net income of 210 million euros, down from 745 million euros in the prior-year period, saying: "The result was significantly impacted by the recording of 845 million euros in loan loss impairment charges, the bulk of which related to the potential economic consequences of the coronavirus crisis."

#ITALY#

UniCredit, an Italian bank, reported that 2Q net income fell 77% on year to 420 million euros, pointing out that trading gains and cost cuts helped to offset declining revenue.

#SWITZERLAND#

Adecco Group, a Swiss human-resources firm, reported that 2Q net income tumbled 87% on year to 21 million euros, citing coronavirus-induced lockdowns. 2Q Adjusted EBITDA sank to 75 million euros from 265 million euros on revenue of 4.18 billion euros, down 29%.

#DENMARK#

Novo Nordisk, a Danish pharmaceutical firm, announced that 2Q net income grew 11% on year to 10.63 Danish kroner and operating profit was up 3% to 13.84 billion Danish kroner. The Company said it now expects full-year operating profit to grow 2-5% at constant exchange rates (vs a growth of 1-5% previously expected).

EX-DIVIDEND

MTU Aero Engines: E0.04, Rio Tinto:119.74p, Unilever: E0.4104, Unilever:36.98p

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM