EU indices significantly down | TA focus on Vonovia

INDICES

Yesterday, European stocks were broadly lower. The Stoxx Europe 600 Index retreated 1.0%, Germany's DAX 30 slid 1.4%, France's CAC 40 fell 0.4% and the U.K.'s FTSE 100 was down 1.5%.

EUROPE ADVANCE/DECLINE

70% of STOXX 600 constituents traded lower or unchanged yesterday.

41% of the shares trade above their 20D MA vs 56% Wednesday (below the 20D moving average).

52% of the shares trade above their 200D MA vs 54% Wednesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 2.4pts to 29.01, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Autos

3mths relative low: none

Europe Best 3 sectors

automobiles & parts, travel & leisure, food & beverage

Europe worst 3 sectors

technology, basic resources, industrial goods & services

INTEREST RATE

The 10yr Bund yield fell 5bps to -0.47% (below its 20D MA). The 2yr-10yr yield spread rose 1bp to -21bps (below its 20D MA).

ECONOMIC DATA

GE 07:00: Jul Factory Orders MoM, exp.: 27.9%

FR 07:45: Jul Budget Balance, exp.: E-124.88B

FR 07:45: Jul Current Account, exp.: E-8.4B

EC 08:30: Aug Construction PMI, exp.: 48.9

FR 08:30: Aug Construction PMI, exp.: 49.4

GE 08:30: Aug Construction PMI, exp.: 47.1

UK 09:00: Aug New Car Sales YoY, exp.: 11.3%

UK 09:30: Aug Construction PMI, exp.: 58.1

EC 16:00: ECB Lane speech

MORNING TRADING

In Asian trading hours, EUR/USD was broadly flat at 1.1848 while GBP/USD edged up to 1.3283. USD/JPY was steady above the 106.00 level. AUD/USD was little changed at 0.7270. This morning, official data showed that Australia's retail sales grew 3.2% on month in July (+3.3% expected).

Spot gold rebounded to $1,936 an ounce.

#UK - IRELAND#

Berkeley Group, a property developer, released a trading update covering the period from May 1 to August 31: "Berkeley's trading has been resilient over this period and supports our existing guidance of £500 million of pre-tax profit for the full year and our commitment to our shareholder returns programme of £280 million per annum. (...) We now anticipate a more even split of profit between the first and second halves of the year, reflecting levels of production that have been better than initially anticipated and our decision not to furlough staff. (...) The value of underlying sales reservations for the first four months of the year is around 20% below the annualised run rate for last year, which is supportive of forward sales remaining around the year-end position of above £1.8 billion. This is a strong position, providing good visibility over the next two years of earnings."

#GERMANY#

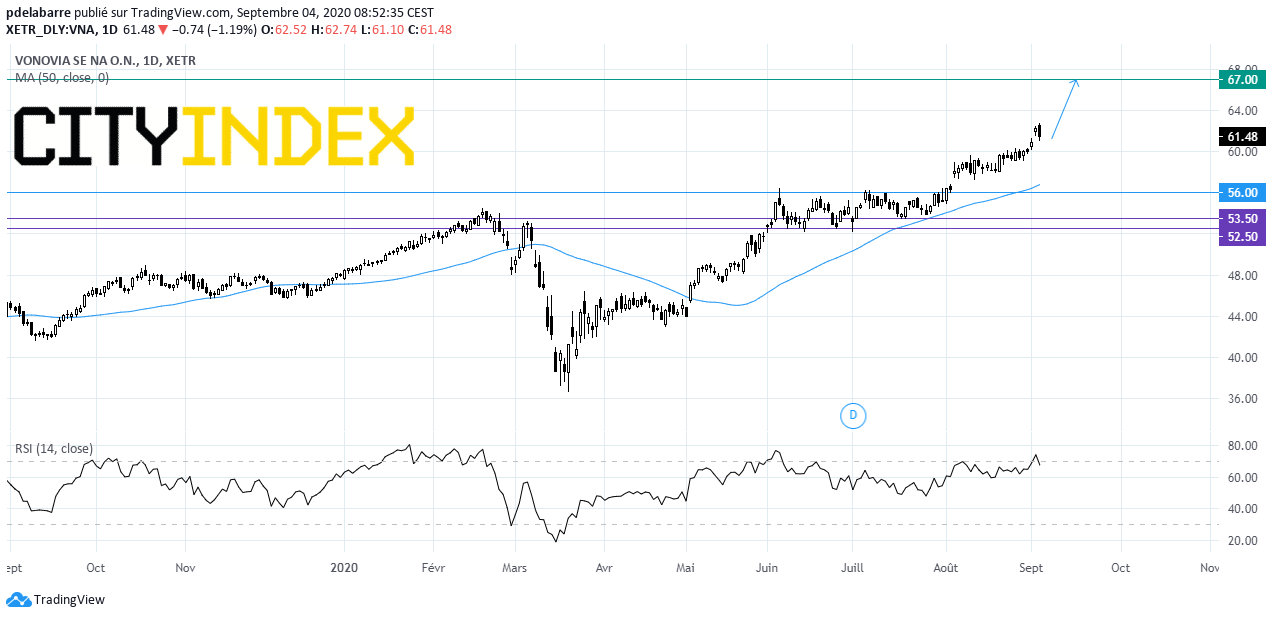

Vonovia, a real estate company, said it will launch a cash capital increase via an accelerated bookbuilding process with a volume of about 1 billion euros. The company added: "The liquidity from this capital increase will be used to repay upcoming debt maturities in the fourth quarter of 2020. The additional proceeds from the issue are to be used for future growth opportunities that arise in the current environment and which Vonovia intends to pursue in line with its investment criteria." From a technical point of view, the previous upward breakout of 56 has triggered a new upmove. Furthermore, prices are supported by the 50-day simple moving average. Above 56, look for 67.

Source: GAIN Capital, TradingView

#FRANCE#

Suez's, an utility company, board has suggested CEO Bertrand Camus to seek alternative offers to Veolia's takeover approach, according to Chairman Philippe Varin cited by BFM Business television.

Pernod Ricard, an alcoholic beverages producer, was downgraded to "neutral" from "buy" at Citigroup.

#SPAIN#

Caixabank, a Spanish bank, reported that it is currently in talks with its peers Bankia to discuss an all-share merger between both institutions.

#FINLAND#

Sampo, a Finnish financial company, was upgraded to "buy" from "hold" at HSBC.

Yesterday, European stocks were broadly lower. The Stoxx Europe 600 Index retreated 1.0%, Germany's DAX 30 slid 1.4%, France's CAC 40 fell 0.4% and the U.K.'s FTSE 100 was down 1.5%.

EUROPE ADVANCE/DECLINE

70% of STOXX 600 constituents traded lower or unchanged yesterday.

41% of the shares trade above their 20D MA vs 56% Wednesday (below the 20D moving average).

52% of the shares trade above their 200D MA vs 54% Wednesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 2.4pts to 29.01, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Autos

3mths relative low: none

Europe Best 3 sectors

automobiles & parts, travel & leisure, food & beverage

Europe worst 3 sectors

technology, basic resources, industrial goods & services

INTEREST RATE

The 10yr Bund yield fell 5bps to -0.47% (below its 20D MA). The 2yr-10yr yield spread rose 1bp to -21bps (below its 20D MA).

ECONOMIC DATA

GE 07:00: Jul Factory Orders MoM, exp.: 27.9%

FR 07:45: Jul Budget Balance, exp.: E-124.88B

FR 07:45: Jul Current Account, exp.: E-8.4B

EC 08:30: Aug Construction PMI, exp.: 48.9

FR 08:30: Aug Construction PMI, exp.: 49.4

GE 08:30: Aug Construction PMI, exp.: 47.1

UK 09:00: Aug New Car Sales YoY, exp.: 11.3%

UK 09:30: Aug Construction PMI, exp.: 58.1

EC 16:00: ECB Lane speech

MORNING TRADING

In Asian trading hours, EUR/USD was broadly flat at 1.1848 while GBP/USD edged up to 1.3283. USD/JPY was steady above the 106.00 level. AUD/USD was little changed at 0.7270. This morning, official data showed that Australia's retail sales grew 3.2% on month in July (+3.3% expected).

Spot gold rebounded to $1,936 an ounce.

#UK - IRELAND#

Berkeley Group, a property developer, released a trading update covering the period from May 1 to August 31: "Berkeley's trading has been resilient over this period and supports our existing guidance of £500 million of pre-tax profit for the full year and our commitment to our shareholder returns programme of £280 million per annum. (...) We now anticipate a more even split of profit between the first and second halves of the year, reflecting levels of production that have been better than initially anticipated and our decision not to furlough staff. (...) The value of underlying sales reservations for the first four months of the year is around 20% below the annualised run rate for last year, which is supportive of forward sales remaining around the year-end position of above £1.8 billion. This is a strong position, providing good visibility over the next two years of earnings."

#GERMANY#

Vonovia, a real estate company, said it will launch a cash capital increase via an accelerated bookbuilding process with a volume of about 1 billion euros. The company added: "The liquidity from this capital increase will be used to repay upcoming debt maturities in the fourth quarter of 2020. The additional proceeds from the issue are to be used for future growth opportunities that arise in the current environment and which Vonovia intends to pursue in line with its investment criteria." From a technical point of view, the previous upward breakout of 56 has triggered a new upmove. Furthermore, prices are supported by the 50-day simple moving average. Above 56, look for 67.

Source: GAIN Capital, TradingView

#FRANCE#

Suez's, an utility company, board has suggested CEO Bertrand Camus to seek alternative offers to Veolia's takeover approach, according to Chairman Philippe Varin cited by BFM Business television.

Pernod Ricard, an alcoholic beverages producer, was downgraded to "neutral" from "buy" at Citigroup.

#SPAIN#

Caixabank, a Spanish bank, reported that it is currently in talks with its peers Bankia to discuss an all-share merger between both institutions.

#FINLAND#

Sampo, a Finnish financial company, was upgraded to "buy" from "hold" at HSBC.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM