U.S Futures consolidating - Watch PFE, BNTX, CRM, WORK, HPE

The S&P 500 Futures are consolidating after they closed higher on Tuesday.

Later today, the Automatic Data Processing (ADP) will post private jobs for November (+0.43 million jobs expected). The Federal Reserve will release its economic report, the Beige Book.

European indices are trying to rebound after a negative open. Pfizer/Biontech Covid-19 vaccine was approved for use in UK and will be available from next week. The German Federal Statistical Office has released October retail sales at +2.6% (vs +1.2% on month expected). The European Commission has posted October PPI at +0.4% (vs +0.2% on month expected) and jobless rate at 8.4%, as expected.

Asian indices closed unchanged. Official data showed that Australia's 3Q GDP fell 3.8% on year, while a 4.4% decline was expected.

WTI Crude Oil is consolidating. The American Petroleum Institute (API) reported that U.S. crude-oil inventories increased 4.15 million barrels in the week ending Nov. 27 (-2.36 million barrels expected). Later today, the International Energy Agency (EIA) will release official crude oil inventories data for the same week (-2.358M expected).

U.S indices closed up on Tuesday, lifted by Technology Hardware & Equipment (+2.65%), Insurance (+2.3%) and Media (+2.27%) sectors.

Gold gains ground as the U.S dollar remains weak on U.S stimulus talks.

Gold rose 8.38 dollars (+0.46%) to 1823.62 dollars.

The dollar index gained 0.1pt to 91.413, slightly rebounding after having hit its lowest level since late April 2018.

U.S. Equity Snapshot

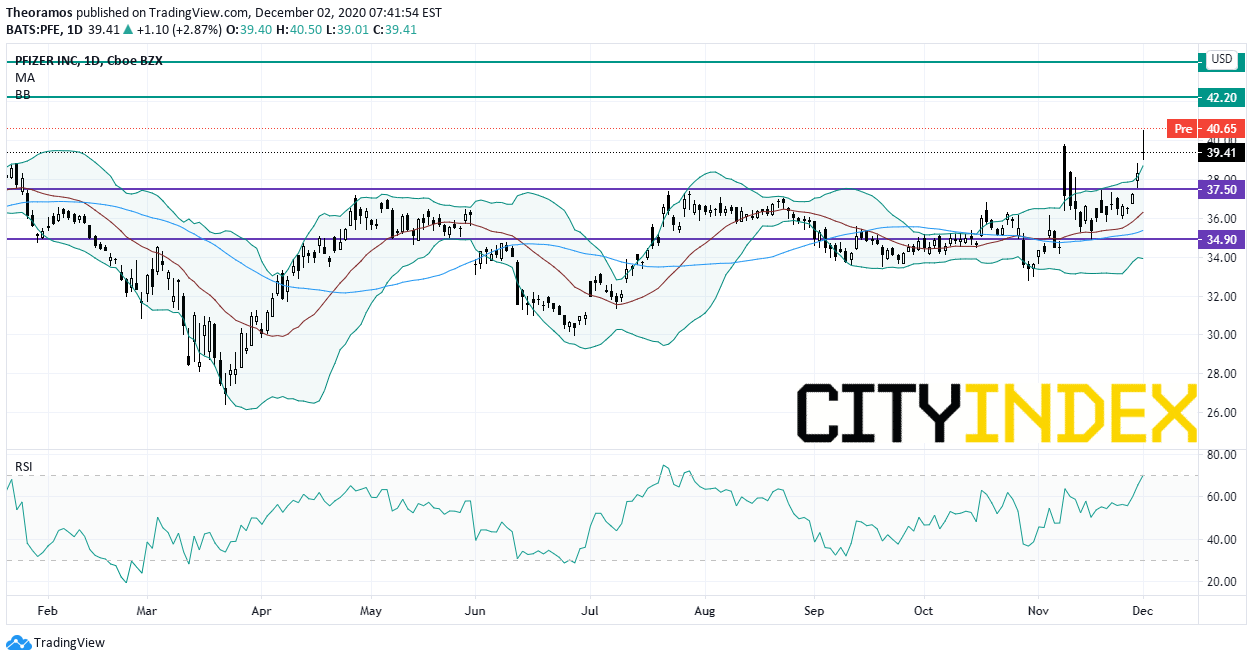

Pfizer (PFE) and BioNTech (BNTX), the pharma, "announced that the Medicines & Healthcare Products Regulatory Agency (MHRA) in the U.K. has granted a temporary authorization for emergency use for their COVID-19 mRNA vaccine (BNT162b2), against COVID-19."

Source: TradingView, GAIN Capital

NetApp (NTAP), a leading provider of data management and storage solutions, announced second quarter adjusted EPS of 1.05 dollar, beating estimates, down from 1.09 dollar a year ago on net sales flat at 1.4 billion dollars, better than expected.

Later today, the Automatic Data Processing (ADP) will post private jobs for November (+0.43 million jobs expected). The Federal Reserve will release its economic report, the Beige Book.

European indices are trying to rebound after a negative open. Pfizer/Biontech Covid-19 vaccine was approved for use in UK and will be available from next week. The German Federal Statistical Office has released October retail sales at +2.6% (vs +1.2% on month expected). The European Commission has posted October PPI at +0.4% (vs +0.2% on month expected) and jobless rate at 8.4%, as expected.

Asian indices closed unchanged. Official data showed that Australia's 3Q GDP fell 3.8% on year, while a 4.4% decline was expected.

WTI Crude Oil is consolidating. The American Petroleum Institute (API) reported that U.S. crude-oil inventories increased 4.15 million barrels in the week ending Nov. 27 (-2.36 million barrels expected). Later today, the International Energy Agency (EIA) will release official crude oil inventories data for the same week (-2.358M expected).

U.S indices closed up on Tuesday, lifted by Technology Hardware & Equipment (+2.65%), Insurance (+2.3%) and Media (+2.27%) sectors.

Approximately 91% of stocks in the S&P 500 Index were trading above their 200-day moving average and 78% were trading above their 20-day moving average. The VIX Index rose 0.2pt (+0.97%) to 20.77 at the close.

On the U.S economic data front, Markit's US Manufacturing Purchasing Managers' Index remained at 56.7 on month in the November final reading (as expected), in line with the November preliminary reading. Finally, Construction Spending rose 1.3% on month in October (+0.8% expected), compared to a revised -0.5% in September.Gold gains ground as the U.S dollar remains weak on U.S stimulus talks.

Gold rose 8.38 dollars (+0.46%) to 1823.62 dollars.

The dollar index gained 0.1pt to 91.413, slightly rebounding after having hit its lowest level since late April 2018.

U.S. Equity Snapshot

Pfizer (PFE) and BioNTech (BNTX), the pharma, "announced that the Medicines & Healthcare Products Regulatory Agency (MHRA) in the U.K. has granted a temporary authorization for emergency use for their COVID-19 mRNA vaccine (BNT162b2), against COVID-19."

Source: TradingView, GAIN Capital

Salesforce.com (CRM), a developer of business software, revealed that it will acquire Slack Technologies (WORK), the collaboration hub, for 27.7 billion dollars. Separately, the company reported third quarter adjusted EPS of 1.74 dollar, up from 0.75 dollar a year ago on revenue of 5.4 billion dollars, up from 4.5 billion dollars a year earlier.

Hewlett Packard Enterprise (HPE), a supplier of information technology products and services, raised its full year 2021 adjusted EPS guidance to 1.60-1.78 dollar vs 1.56-1.76 dollar previously.NetApp (NTAP), a leading provider of data management and storage solutions, announced second quarter adjusted EPS of 1.05 dollar, beating estimates, down from 1.09 dollar a year ago on net sales flat at 1.4 billion dollars, better than expected.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM