US Futures sliding, watch FDX, AAPL, FB, BYND

The S&P 500 Futures are losing ground, after Tuesday up move, due to a strong rally in the final moment of the trading session.

Due later today the U.S. Commerce Department will report construction spending in May. The Automatic Data Processing (ADP) will release June private jobs report. The Institute for Supply Management will post its Manufacturing Index for June. The Federal Reserve will release its latest FOMC meeting minutes.

Asian indices ended mixed. The Japanese Nikkei dropped 0.75% as Tankan Large Enterprises Manufacturing Index slid to -34 in the second quarter (-31 expected) from -8 in the first quarter, and the Large Enterprises Non-manufacturing Index fell to -17 in the second quarter (-20 expected) from 8. On the other side, China Mainland CSI 300 bounced 2.01% and Australian ASX 200 added 0.62% as China's Caixin Manufacturing PMI rose to 51.2 in June (50.5 expected) from 50.7 in May. Hong Kong market was closed for Hong Kong Special Administrative Region Establishment Day.

WTI Crude Oil futures are gaining some ground The American Petroleum Institute (API) reported that U.S. crude oil stockpile dropped 8.2M barrels for week ended June 26, that’s the largest decline recorded since August 2019. Later today, EIA will release crude oil inventories data for last week.

Gold consolidates after having reached its highest price in nearly eight years on economic fears.

Gold fell 0.83 dollar (-0.05%) to 1780.13 dollars.

The US dollars edges up before the release of major economic data.

EUR/USD fell 45pips to 1.1189 while GBP/USD declined 24pips to 1.2377.

Due later today the U.S. Commerce Department will report construction spending in May. The Automatic Data Processing (ADP) will release June private jobs report. The Institute for Supply Management will post its Manufacturing Index for June. The Federal Reserve will release its latest FOMC meeting minutes.

European indices are dropping. On the statistical front, German Unemployment Rate rose to 6.4% in June from an expected 6.5% and 6.3% in May. The number of unemployed rose by 69,000, after an increase of 237,000 (revised from 238,000) the previous month. It was expected to rise by 120,000. Several PMI have been released across Europe: in the euro area, the PMI manufacturing index came out at 47.4 in June as a second estimate, compared with 46.9 in the first and 39.4 in May. German Index came out at 45.2 in second reading compared to 44.6 in the first estimate and 36.6 the previous month. In France, the PMI Manufacturing index came out at 52.3 in June as a second estimate, compared to 52.1 in the first reading and 40.6 in May. In the United Kingdom, the PMI manufacturing index was confirmed at 50.1 as a second estimate for June, compared to 40.7 the previous month.

Asian indices ended mixed. The Japanese Nikkei dropped 0.75% as Tankan Large Enterprises Manufacturing Index slid to -34 in the second quarter (-31 expected) from -8 in the first quarter, and the Large Enterprises Non-manufacturing Index fell to -17 in the second quarter (-20 expected) from 8. On the other side, China Mainland CSI 300 bounced 2.01% and Australian ASX 200 added 0.62% as China's Caixin Manufacturing PMI rose to 51.2 in June (50.5 expected) from 50.7 in May. Hong Kong market was closed for Hong Kong Special Administrative Region Establishment Day.

WTI Crude Oil futures are gaining some ground The American Petroleum Institute (API) reported that U.S. crude oil stockpile dropped 8.2M barrels for week ended June 26, that’s the largest decline recorded since August 2019. Later today, EIA will release crude oil inventories data for last week.

Gold consolidates after having reached its highest price in nearly eight years on economic fears.

Gold fell 0.83 dollar (-0.05%) to 1780.13 dollars.

The US dollars edges up before the release of major economic data.

EUR/USD fell 45pips to 1.1189 while GBP/USD declined 24pips to 1.2377.

US Equity Snapshot

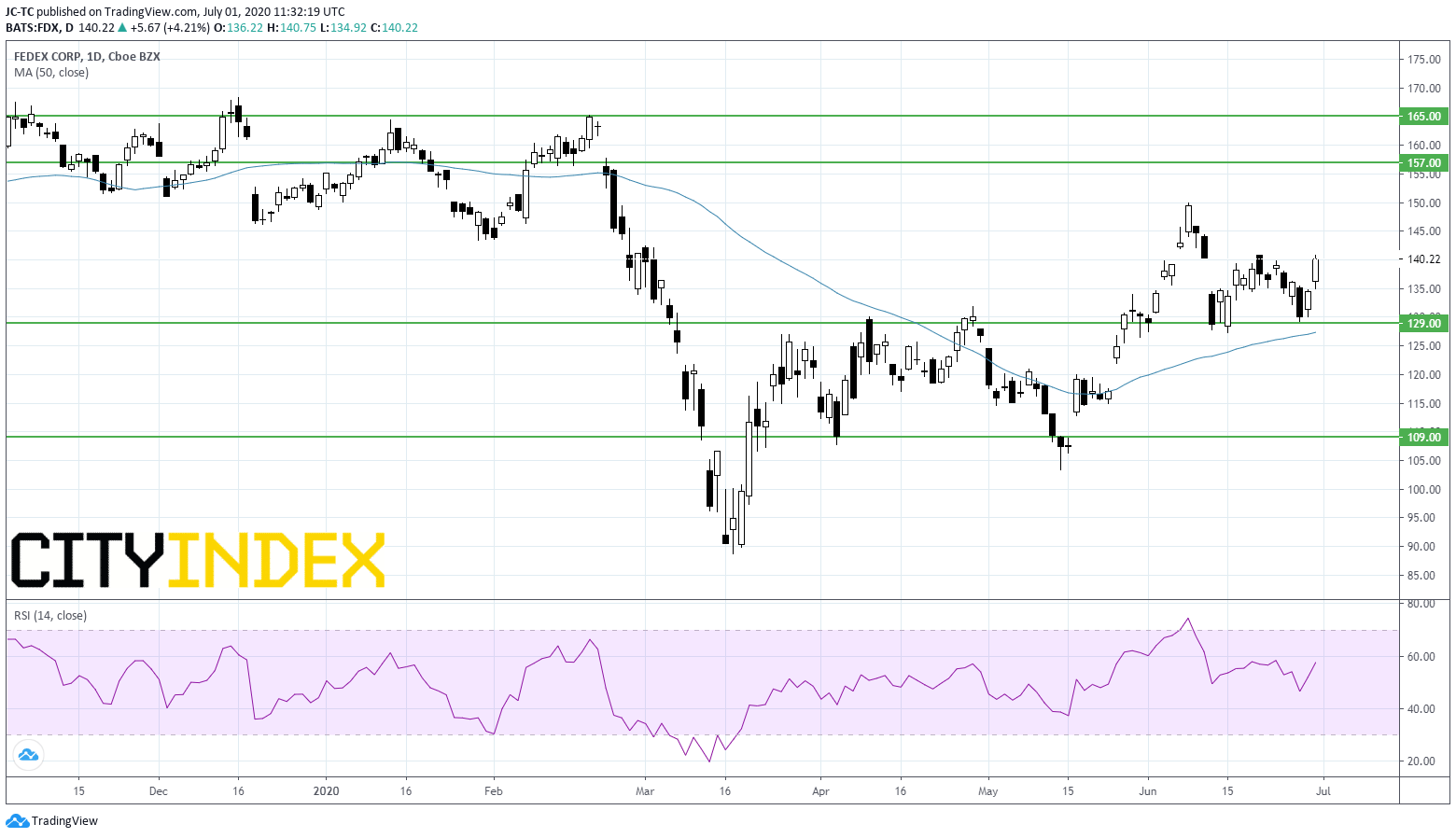

FedEx (FDX), the package delivery service company, disclosed fourth quarter adjusted EPS of 2.53 dollars, significantly above forecasts, down from 5.01 dollars a year ago, on revenue of 17.4 billion dollars, better than expected, down from 17.8 billion dollars last year. Shares jumped after hours following that release. Peer UPS (UPS) also gained ground.

Apple (AAPL) target price was raised to 390 dollars from 325 dollars at Independent Research.

Facebook (FB): retailer Target (TGT) suspended ads on Facebook and Instagram for July.

Beyond Meat (BYND), a producer of plant-based meat substitutes, surged in extended trading after announcing a partnership with Alibaba to start selling its meatless burger patties in mainland China.

General Mills (GIS), a packaged food company, reported fourth quarter adjusted EPS up 33% to 1.10 dollar, on sales up 21% to 5 billion dollars. Both figures beat estimates.

Macy's (M), the department store chain, posted first quarter adjusted LPS of 2.03 dollars, beating estimates, vs an EPS of 0.44 dollar a year earlier.

Capri Holdings (CPRI), an owner of multiple luxury apparel brands, posted fourth quarter sales down 11.3%. Company's fourth quarter ended on March 28. Capri expects first quarter sales to be down 70% and sees a significant loss for the same period.

Caterpillar (CAT), the world's largest manufacturer of heavy equipment for multiple industries, and Deere & Co (DE), a manufacturer of agricultural and construction equipment, were both upgraded to "buy" from "not rated" at Deutsche Bank.

Source : TradingView, Gain Capital

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM