EU indices try to rebound | TA focus on Enel

INDICES

Yesterday, European stocks were broadly under pressure. The Stoxx Europe 600 declined 1.0%, Germany's DAX fell 0.3%, France's CAC 40 slid 1.4%, and the U.K.'s FTSE 100 sank 1.6%.

EUROPE ADVANCE/DECLINE

67% of STOXX 600 constituents traded lower or unchanged yesterday.

70% of the shares trade above their 20D MA vs 75% Friday (above the 20D moving average).

84% of the shares trade above their 200D MA vs 85% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 2.84pts to 22.91, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Financial Services

3mths relative low: none

Europe Best 3 sectors

automobiles & parts, basic resources, technology

Europe worst 3 sectors

energy, financial services, health care

INTEREST RATE

The 10yr Bund yield was unchanged to -0.59% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -17bps (above its 20D MA).

ECONOMIC DATA

GE 08:00: Oct Unemployment Rate Harmonised, exp.: 4.5%

UK 08:00: Nov Nationwide Housing Prices YoY, exp.: 5.8%

UK 08:00: Nov Nationwide Housing Prices MoM, exp.: 0.8%

FR 09:50: Nov Markit Manufacturing PMI final, exp.: 51.3

GE 09:55: Nov Unemployment Rate, exp.: 6.2%

GE 09:55: Nov Unemployment chg, exp.: -35K

GE 09:55: Nov Markit Manufacturing PMI final, exp.: 58.2

EC 10:00: Nov Markit Manufacturing PMI final, exp.: 54.8

UK 10:30: Nov Markit/CIPS Manufacturing PMI final, exp.: 53.7

EC 11:00: Nov Inflation Rate YoY Flash, exp.: -0.3%

EC 11:00: Nov Core Inflation Rate YoY Flash, exp.: 0.2%

EC 11:00: Nov Inflation Rate MoM Flash, exp.: 0.2%

FR 11:00: Nov New Car Registrations YoY, exp.: -9.5%

MORNING TRADING

In Asian trading hours, EUR/USD rebounded to 1.1958 and GBP/USD advanced to 1.3357. USD/JPY held gains at 104.40. This morning, government data showed that Japan's jobless rate rose to 3.1% in October (as expected) from 3.0% in September, while capital spending dropped 10.6% on year in the third quarter (-12.1% expected). AUD/USD bounced to 0.7366. Earlier today, the Reserve Bank of Australia kept its benchmark rate unchanged at 0.10% as expected. RBA reiterated that it "is not expecting to increase the cash rate for at least 3 years".

Spot gold climbed to $1,785 an ounce.

#UK - IRELAND#

AstraZeneca, a pharmaceutical giant, said it has agreed to sell the rights to Crestor (rosuvastatin) and associated medicines in over 30 countries in Europe, except the U.K. and Spain, to Grunenthal GmbH for an initial price of 320 million dollars plus future milestone payments of up to 30 million dollars.

EasyJet, a budget airline, was upgraded to "neutral" from "sell" at Goldman Sachs.

Wizz Air, a low-cost airline company, was downgraded to "sell" from "neutral" at Goldman Sachs.

#GERMANY#

Allianz, a financial services group, will acquire Australian bank Westpac's general insurance business for more than 500 million Australian dollars, reported the Australian Financial Review.

Henkel, a chemical and consumer goods company, was upgraded to "buy" from "hold" at HSBC.

Symrise, a producer of flavours and fragrances, was upgraded to "buy" from "neutral" at UBS.

#FRANCE#

Pernod Ricard, an alcoholic beverages producer, was upgraded to "buy" from "hold" at Deutsche Bank.

#BENELUX#

AB InBev, a drink and brewing company, was downgraded to "hold" from "buy" at Deutsche Bank.

#ITALY#

UniCredit, an Italian bank, said CEO Jean Pierre Mustier will be retiring from his role at the end of his mandate which expires in April 2021.

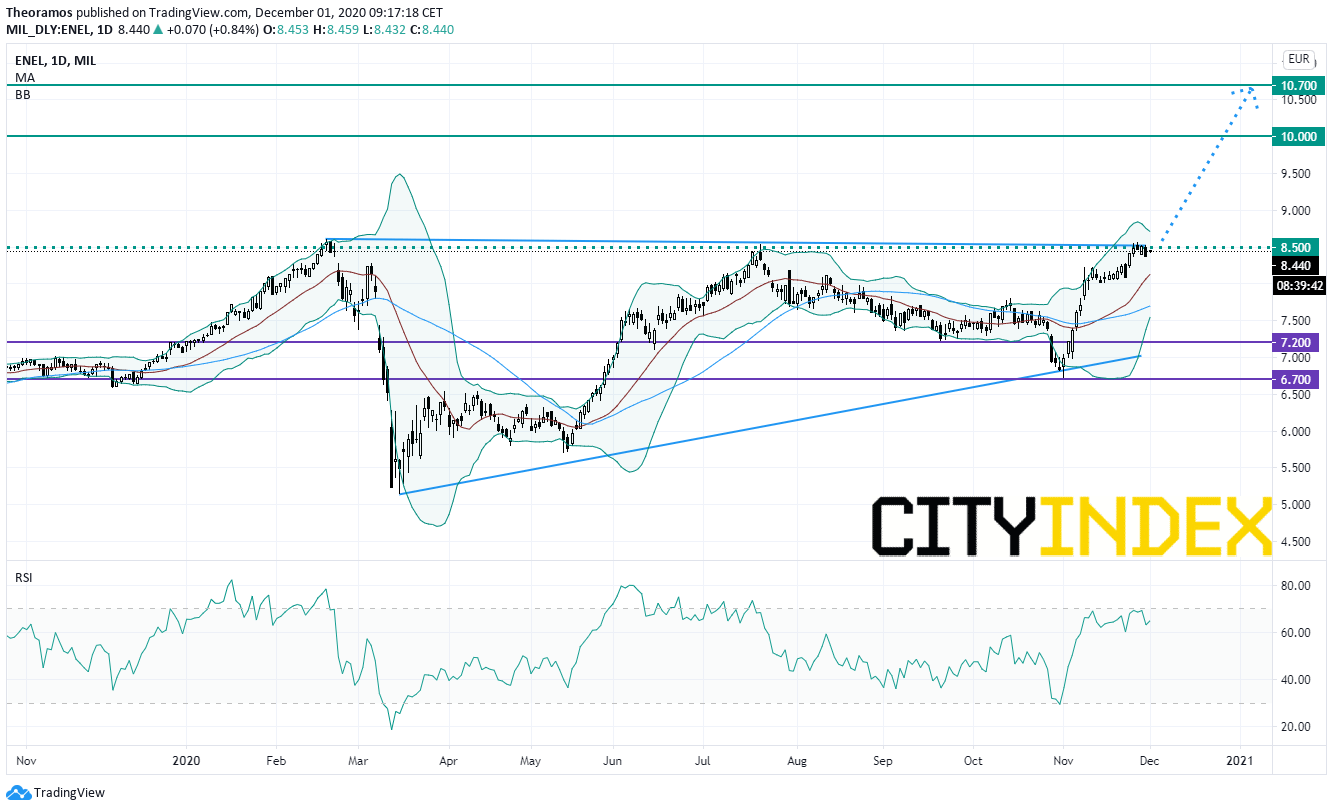

Enel, an Italian energy group, was upgraded to "buy" from "hold" at HSBC.

From a technical point of view, the stock is trading within a symmetrical triangle since February 2020. A daily close above the key horizontal resistance at 8.5E would trigger a new up leg towards 10E and 10.7E in extension.

LVMH: E2

Yesterday, European stocks were broadly under pressure. The Stoxx Europe 600 declined 1.0%, Germany's DAX fell 0.3%, France's CAC 40 slid 1.4%, and the U.K.'s FTSE 100 sank 1.6%.

EUROPE ADVANCE/DECLINE

67% of STOXX 600 constituents traded lower or unchanged yesterday.

70% of the shares trade above their 20D MA vs 75% Friday (above the 20D moving average).

84% of the shares trade above their 200D MA vs 85% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 2.84pts to 22.91, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Financial Services

3mths relative low: none

Europe Best 3 sectors

automobiles & parts, basic resources, technology

Europe worst 3 sectors

energy, financial services, health care

INTEREST RATE

The 10yr Bund yield was unchanged to -0.59% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -17bps (above its 20D MA).

ECONOMIC DATA

GE 08:00: Oct Unemployment Rate Harmonised, exp.: 4.5%

UK 08:00: Nov Nationwide Housing Prices YoY, exp.: 5.8%

UK 08:00: Nov Nationwide Housing Prices MoM, exp.: 0.8%

FR 09:50: Nov Markit Manufacturing PMI final, exp.: 51.3

GE 09:55: Nov Unemployment Rate, exp.: 6.2%

GE 09:55: Nov Unemployment chg, exp.: -35K

GE 09:55: Nov Markit Manufacturing PMI final, exp.: 58.2

EC 10:00: Nov Markit Manufacturing PMI final, exp.: 54.8

UK 10:30: Nov Markit/CIPS Manufacturing PMI final, exp.: 53.7

EC 11:00: Nov Inflation Rate YoY Flash, exp.: -0.3%

EC 11:00: Nov Core Inflation Rate YoY Flash, exp.: 0.2%

EC 11:00: Nov Inflation Rate MoM Flash, exp.: 0.2%

FR 11:00: Nov New Car Registrations YoY, exp.: -9.5%

MORNING TRADING

In Asian trading hours, EUR/USD rebounded to 1.1958 and GBP/USD advanced to 1.3357. USD/JPY held gains at 104.40. This morning, government data showed that Japan's jobless rate rose to 3.1% in October (as expected) from 3.0% in September, while capital spending dropped 10.6% on year in the third quarter (-12.1% expected). AUD/USD bounced to 0.7366. Earlier today, the Reserve Bank of Australia kept its benchmark rate unchanged at 0.10% as expected. RBA reiterated that it "is not expecting to increase the cash rate for at least 3 years".

Spot gold climbed to $1,785 an ounce.

#UK - IRELAND#

AstraZeneca, a pharmaceutical giant, said it has agreed to sell the rights to Crestor (rosuvastatin) and associated medicines in over 30 countries in Europe, except the U.K. and Spain, to Grunenthal GmbH for an initial price of 320 million dollars plus future milestone payments of up to 30 million dollars.

EasyJet, a budget airline, was upgraded to "neutral" from "sell" at Goldman Sachs.

Wizz Air, a low-cost airline company, was downgraded to "sell" from "neutral" at Goldman Sachs.

#GERMANY#

Allianz, a financial services group, will acquire Australian bank Westpac's general insurance business for more than 500 million Australian dollars, reported the Australian Financial Review.

Henkel, a chemical and consumer goods company, was upgraded to "buy" from "hold" at HSBC.

Symrise, a producer of flavours and fragrances, was upgraded to "buy" from "neutral" at UBS.

#FRANCE#

Pernod Ricard, an alcoholic beverages producer, was upgraded to "buy" from "hold" at Deutsche Bank.

#BENELUX#

AB InBev, a drink and brewing company, was downgraded to "hold" from "buy" at Deutsche Bank.

#ITALY#

UniCredit, an Italian bank, said CEO Jean Pierre Mustier will be retiring from his role at the end of his mandate which expires in April 2021.

Enel, an Italian energy group, was upgraded to "buy" from "hold" at HSBC.

From a technical point of view, the stock is trading within a symmetrical triangle since February 2020. A daily close above the key horizontal resistance at 8.5E would trigger a new up leg towards 10E and 10.7E in extension.

Source: TradingView, GAIN Capital

LVMH: E2

Latest market news

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM